Trillions to financial Terra Incognita; So far very little for ordinary Americans

By Sherman DeBrosse / The Rag Blog / January 8, 2008

At this moment, the cost of the bailouts, including guarantees, stands at $ 7.2 billion. That includes a $600 billion guarantee for money market funds, $200 billion so far for credit card issuers, $345 to Citigroup, the Fanny and Freddy loans, $200 billion for hedge funds, and on and on and on. Now we hear that the remaining $350 billion from the Troubled Assets Recovery Program has already been committed.

This writer has spent several weeks trying to find one person who could coherently explain why so much money had to be spent covering bad investments that are nearly impossible to understand. No one came forward.

Yes, the money for AIG and a few investment house bailouts were probably necessary because they involved bad securities Americans peddled abroad to people in nations who were accustomed to responsible regulations and did not know casino economics reigned supreme here. It was a matter of joining a joint effort in propping up the international financial system.

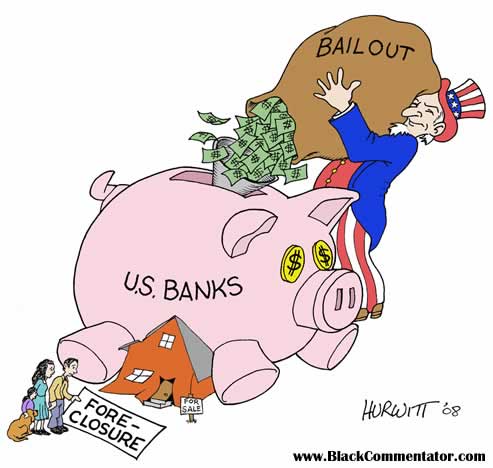

Covering the Bets of the Rich

What about trillions committed to banks and banking houses that have not been satisfactorily explained and justified? One of the people I respect most pointed out that we were talking about two economies, one we more or less understand, and the other being the terra incognita of the private casinos of the rich. The Treasury refuses to tell us who gets the remaining $350 billion of TARP, and many of the known recipients refuse to tell how the money was used.

Until someone in Washington begins to explain what is going on, we should be prepared to assume the worst. We have incurred trillions in obligations to cover the bets of the wealthy and keep their private casinos open. None of this resulted in making much more money available for ordinary loans. It is true that some of our pension funds are heavily invested in the hedge funds and derivatives.

Without some explanations, our representatives in Congress should be demanding that no more FED obligations or TARP assets be invested in covering exotic economic transactions. It would be far less expensive to prop up some pension funds than to ship off more money into terra incognita. It is also important to put the trillions of guarantees on hold or drag out indefinitely making good on those promises. First someone should assign verifiable values to all the ethereal financial instruments that have been guaranteed. We all recall in the previous S and L crisis how the culprits were able to repurchase seized assets at pennies on the dollar from the Resolution Trust Corporation.

Let’s Look at the Pig in the Poke

The next administration must take a close look at the loans and guarantees that have already been made and find ways to use them to serve the interests of most Americans. It seems that the TARP money was largely invested in warrants and senior preferred stock. We know far less about what the FED money gained for the taxpayers. In both cases, there should be federal representative on the boards of assisted banks and brokerage firms. Recipients who do not resume normal commercial loans must feel some pain, perhaps inflicted through the tax code.

The banks and financial institutions live in both worlds — terra incognita and the ordinary world of goods and services. So far, the U.S. government has only moved to cover the bets of the big players in the casino. The Democratic Congress has generously bailed out the capitalist system and purchased what appears to be a “pig in a poke” for the taxpayer. I’s no wonder consistent progressives are so often to abandon the Democrats.

Address Suffering in the Real World

Now is the time to address the economic concerns of ordinary people in a financial world we all more or less understand. Congress and the spokesmen for the big money players must be reminded that their long term survival depends on their utility to the American economy.

Funds were extended to banks and the financial services industry with the expectation that credit would again be available to turn the wheels of the economy. But little happened. At first, most of us assumed the recipients of federal money were sitting on these funds because they were covering still more bad debt. There is probably some truth here. We all know that the CPI fell by the greatest amount in 62 months in November and that it still is plunging. The bankers are using our money to cover their balance sheets because they fear a certain amount of deflation is coming and that it will be followed by inflation in several years. We have the twin deficit crises — federal debt and the balance of payments — coupled with a dishonest, Wild West financial industry. Even commercial banks have become high risk operations. The instability of the system and the real threats of deflation and inflation account for why lenders are holding their cards near their chests and the wealthy in record numbers are shipping money overseas.

Free Up Credit

To ward off deflation and eventual inflation, banks must return normal commercial activity now, and the taxpayers need to establish an insurance program for responsible loans. AIG, the taxpayers’ new asset, can be put to use here. Above all, the mortgage crisis must be stemmed to avert a deflationary plunge. One fifth of home mortgages are under water — meaning the value of the mortgaged homes is less than what is owed. Initially,12% of outstanding mortgages were in deep trouble. That number is growing. Housing prices continue to plummet as deflationary forces begin to take hold. Deflation is not a certainty at this point, but it is a possibility that grows with each day of flat consumer spending and inactive credit markets.

The banks are refinancing about 200,000 homes a month. To do more, they need a program that guarantees existing bad housing loans and incentives to greatly accelerate the process. People who are able to handle their mortgages might stop making payments if they see other folks get stabilization deals that are too good. For that reason, the stabilization loans should be for at least 35 years, and interest rates must be at a level to discourage new and unnecessary foreclosures. If there is any appreciation on a covered house, the federal government must receive a piece of it in return for the guarantee. The program would probably have to exclude mortgages that are more than $150,000 under water, unless the banks agreed to swallow some of the loss.

If commercial lending institutions are afraid to participate, use the various federal housing programs to buy up the paper and rewrite the loans. Every month that is wasted adds momentum to deflation. During the New Deal, the Home Owners Loan Corporation saved one in five home owners. The mission was to save people, not banks. We, the people may lose some money, but it will not be the trillions that will disappear by underwriting bad paper in terra incognita. Sheila Bair, head of the FDIC, would be the ideal housing czar to supervise this massive guarantee program.

How Much of a Recovery Can there be Without a Reinvigorated Industrial Sector?

Other decisions about what to do about restoring economic health should be made with the knowledge that we have relied on bubbles in the past to revive the economy. There are no new ones on the horizon, and reliance on bubbles is unhealthy in the long run. The green economy is a necessary and good thing, but many are mistaken in believing it will be an engine powerful enough to make Americans again the consumers of last resort for the entire world. The economy will not recharge itself with a surge in the service and information industries. They still are not large enough to accomplish that. The simple fact is that the industrial sector is essential to recovery — and this means automobiles and heavy industry. European governments understand this and are moving to assist their automakers with loans in the neighborhood of $50 billion.

The debate over the auto industry loan has been fascinating and has revealed a great deal of mendacity and downright ugly attitudes. All sorts of factual matters were distorted. Yes, the domestic industry made many bad decisions, and labor agreements gave workers more than most Americans thought appropriate. But the fact is that the domestic industry was close to bringing labor costs into line, moving legacy costs over to the unions, and dealing with other fundamental issues. Those who advocated Chapter 11 bankruptcy overlooked the fact that the process would be long and tedious and that there would be no private lenders out there with money to but the Big Three back together. Like Chapter 7, it would be a death sentence. Letting the Big Three sink would amount to an irreversible decision to give up on any serious plans to revitalize the manufacturing sector. Those, led by short-sighted Southern senators, who want to destroy the UAW and the Big Three overlook what the wreckage would cost the taxpayers in unemployment benefits for three million people, welfare benefits, decreased income tax revenue, and federal assumption of retirement fund obligations.

There must be a stimulus plan for restructuring the domestic auto industry. In addition to strict accountability components, it might include generous federal assistance to the Big Three’s lending agencies, making it possible for people to acquire new, fuel efficient vehicles with 3% loans. A higher but still advantageous rate would be assigned to the existing inventory of less efficient vehicles. Directly provide them with the funds to make car loans. We are now considering the possibility that 16 million vehicle sales years may never be restored. Federal assistance, through the Big Three, for car loans might rekindle Americans’ love affairs with cars.

Yes, the UAW will have to bite the bullet again. Excess production capacity could be acquired by the federal government and sold or leased bit by bit, in very sweet deals, to small industries with long term-growing pains — outfits that need space but cannot afford to build. Some of the capacity could be used to help build rapid transit and public transportation equipment and machinery and to start restoring the military inventories depleted by two wars.

Rebuilding the American manufacturing sectors will require lowering employer benefit costs, and that can only be done by providing a universal health plan unburdened with successive pharmaceutical costs and insurance company profits. It would be good to pass this now, but it might require a much deeper recession before enough Congressmen acquire enough courage to vote in the interests of most of their constituents.

Consideration should also be given to a Value Added Tax as a means of leveling the playing field among countries that adhere to the General Agreement on Trade and Tariffs. Unfortunately, that is a regressive approach, but is used by our competitors and there seems to be no other approach that works as well to help domestic producers. Given the likelihood of millions more lost jobs in 2009 and 2010, now is the time to consider this.

Of President-Elect Obama’s stimulus package, it appears that $300 million will go to tax cuts — a bow to University of Chicago economics, and $400 billion to the kinds of project that will create assets, work , and send money coursing through the economy. The latter is a tip of the hat to John Maynard Keynes’s economics.

The New Deal Example

Much has been said of late about how FDR’s deployment of Keynes did not end the Great Depression. The fact is that he did not spend enough on pump priming. Before becoming president, he read a book popularizing Keynes, and he scrawled in it something to the effect that you do not get something for nothing. FDR should have spent a lot more because ordinary people no longer had the ability to recharge the economy because there was an inequitable distribution of income. The depression lasted so long due to under-consumption and maldistribution of income. The $300 billion in tax cuts, mostly for ordinary folks, will not accomplish a great deal even if government succeeds in getting the money out fast, perhaps through sharp cuts in FICA deductions.

Those discussing the New Deal example forget that Roosevelt took some steps to deal with inequities in income, particularly by backing unions. That helped prevent economic downturns due to under consumption. It is doubtful if the national climate is such as to make progress on this front possible.

The key is in the pump-priming initiatives, and it is possible that this two year package is too small. The Obama Administration might be in danger of repeating the New Deal’s mistake. The stimulus plan must have a component to rebuild American industry, and that will be costly. There must be enough money borrowed and committed now, while other nations are still taking shelter in Treasury bonds and willing to lend. Our advantage is in being able to borrow at rates far less than those at which we lend. This situation will not last much longer as the world’s monetary situation is due for drastic changes that will not be to our long-term best interest. If the world monetary situation shifts in the direction most expect, we had better have a healthy and productive manufacturing sector or accept the consequences of long-term decline across many fronts.

It will require a number of pieces of separate legislation to implement these plans. We progressives will be facing a four year campaign in putting out accurate information about economic policy if the Obama administration is to prevail in heading off a depression. Already the Republican leadership has signaled that the GOP will delay the stimulus package. It would be a great mistake to promise Republicans up front that concessions would be forthcoming on new estate tax legislation or that the tax cuts for the rich can continue another year. Republicans have 42 more or less disciplined votes and the not-so covert help of a handful of Democratic conservatives in the Senate. It is possible that Mitch McConnell and his minions will be in a position to stop whatever they wish without fear of being punished by the voters. Most of them are in safe red states, and their leaders know that odds are Republicans could pick up seats in 2010, as the opposition party usually gains in off-year elections.

[Sherman DeBrosse, the pseudonym for a retired history professor, is a regular contributor to The Rag Blog and also blogs at Sherm Says and on DailyKos.]

ha,ha wait till you see the story I just fwdd to the blog editors — here comes a bailout for the “common guy”, nudge nudge wink!!

Catholics destroyed American industry: Palmisano, Grasso, Damato, Langone, Dioguardi, Ranieri. The subprime construction mobsters had hookers deliver the mortgages to the banks. McCain’s Keeting started it all. They find American cars too advanced for them to use or their mechanics to fix. Their slovenly, anti-intellectual work ethic produces vacuous, casuistrous blather. Ellis Island Popeholes brought in FDR. Carolignian Brzezinski spawned Zia al Haq, Khomeini, and bin Laden – breaks up superpowers via Aztlan and Kosovo as per Joel Garreau’s Nine Nations. Brzezinski, Buckley and Buchanan winked anti-Semitic votes for Obama, delivered USA to Pope’s feudal basket of Bamana Republics. Michael Pfleger and Joe Biden prove Obama is the Pope’s boy. Talal got Pontifical medal as Fatima mandates Catholic-Muslim union against Jews (Francis Johnson, Great Sign, 1979, p. 126), Catholic Roger Taney wrote Dred Scott decision. John Wilkes Booth, Tammany Hall and Joe McCarthy were Catholics. Now Catholic majority Supreme Court. NYC top drop outs: Hispanic 32%, Black 25%, Italian 20%. NYC top illegals: Ecuadorean, Italian, Polish. Ate glis-glis but blamed plague on others, now lettuce coli. Their bigotry most encouraged terror yet they reap most security funds. Rabbi circumcizes lower, Pope upper brain. Tort explosion by glib casuistry. Bazelya 1992 case proves PLO-IRA-KLA links.