The estimate of three years of easily affordable driving depends primarily on how long the current fracking boom, which is holding down the global oil price, can be sustained.

Drive, he said. Photo by David Pardo / AP.

Second in a series

Part 1 of this series stirred up a lot of interest with Rag Blog readers, and it was reposted by Resilience.org where it was also popular. I imagine the article’s somewhat alarming title struck a nerve, calling attention to the repressed fears that challenge our suburban, car-centric American culture. Fears that stem from our culture of denial in response to business as usual.

In Part 2 we will further explore the constraints on our energy resources and will look at the role of finance capital in perpetuating our denial; denial that inhibits energy reform until there is a full blown crisis.

Below are clickable section heads for those of you who like to jump around.

- The context of our driving problem

- Fracking looks like a fossil fuel retirement party

- An oil glut for now

- We are now at the doorstep of globally peaking oil

- Expert evidence for three more years of easily affordable driving

- Why fuel prices probably won’t fall much more

- A timeless pattern of energy investment overshoot

- Military events which could seriously interfere with driving in less than three years

- Economic events which could seriously interfere with driving in less than three years

- Part 3 of “America: You’ve got three more years to drive normally!.”

The context of our driving problem

As a nation we know that something is deeply wrong, starting with a politically gridlocked congress. The recent march against climate change underlined this high level of public concern.

Arguably the top issue of our times has become how long our physically expansive system of global finance capital can maintain profitable growth without wrecking the global environment. In this respect, public attention to global warming has become the leading example.

Business as usual justifies its legitimacy by maintaining that at least some plausibly improved version of our system can pay off its immense deficit of public and private debt by growing profitably forever. And can do so in a finite world that is clearly already struggling to deal with a human population of 7 billion. There is now a wealth of solid scientific research and useful information that shows that this goal is impossible; information easily available from a growing assortment of environmental awareness sites like the Post Carbon Institute.

Expansionist economic control and free market fundamentalism have become like a state religion.

Expansionist economic control and free market fundamentalism have become like a state religion uniting politics and economics in support of corporate domination. In accord with this point of view, it comes as no surprise to see Paul Krugman, a liberal Keynesian advocate of a gentler greener kind of capitalist economics, blame the Post Carbon Institute for teaching about natural limits to economic growth.

This recent exchange features Krugman as an economic expansionist, and Richard Heinberg, in response, laying out conflicting positions on the growth issue. Nobel economics prize winner Krugman seems to have blundered into an uphill debate against top scientists and their intellectual allies.

Now, with the help of recent geological data, we can see that peak oil will probably soon limit and affect an important aspect of American life, namely our driving. The global oil supply situation will probably only permit about three more years of easily affordable driving. So far we have been able mostly to ignore this problem, which has been nipping at our heels for most of the past decade by more than tripling oil prices.

Follow the oil

Oil, when burned, has the unique ability to supply the motive muscle power needed throughout our global civilization. The power to move stuff around; to physically expand global trade by powering nearly all the world’s ships, planes, trucks, and trains. The Hirsch report laid out the difficulty of an economic transition away from oil about a decade ago, by predicting the need for about 20 years to properly prepare for peak oil. Everyone has become fond of solar panels these days, but there has not been nearly enough progress towards alternatives since conventional oil peaked in 2005, given the true scale of the problem.

Peak oil is here, or close enough for us to be able to sketch out important details.

Peak oil is here, or close enough for us to be able to sketch out important details. The current world oil glut is genuine, and we need to try to see why this situation is actually quite compatible with a globally peaking oil supply. We can closely examine the considerable body of evidence that suggests about three more years of easy driving. Anyone can study the same evidence and attempt a more optimistic interpretation.

Thanks to what could be seen as the increasingly disruptive side effects of maintaining our globally oil-dependent economy, we face unpredictable problems that could interfere with normal driving even sooner than three years.

Having made a horrible mess of Iraq, we now see rising conflict throughout the Middle East, largely as a result of an old agreement with the Saudis after the 1970s energy crisis. An agreement to maintain through military force the stable production and export of OPEC oil on the world marketplace. A second looming threat stems from the fact that the global economy was thoroughly disrupted by a severe oil price spike in 2008 and has not recovered. The world of finance capital has been kept solvent since then through transfusions of publicly funded credit, such as quantitative easing and low interest rates.

It is no accident that we sometimes call our dollars petrodollars. The British pound may have been backed by gold, but now our dollar is backed by its singular ability to buy oil and its combustion-derived mobile power on the global market. Oil is only globally traded in dollars, which are also the world’s standard reserve currency.

Our dollar-based global economy, led by finance capital centered in Wall Street and London, has managed to function successfully since WWII, but, distressingly, it is beginning to resemble an oil-addictive dollar-based global Ponzi scheme, sure to fail without an exponential growth in profit.”

Fracking looks like a fossil fuel retirement party

The technical advance that is keeping the USA driving affordably, for now at least, is hydrofracturing or fracking, used to produce tight gas and oil from shale deposits. This U.S. fracking boom is now adding more than 3 million barrels of tight oil and closely associated liquid condensate fuel each day. This is enough new product that, when it is added to the world’s slowly declining conventional oil production, the resulting in obscuring and delaying the onset of the peak oil problem, if only for a few years.

For the moment, there is a global oil glut and a falling price due to an unusually weak global customer demand for the relatively constant stream of oil being produced and consumed globally, but that does not mean that this product is being produced at a profit. Over the short run, shifting consumer demand due to the economy or freezing weather conditions can have a much bigger faster effect on price than investment in new production, which is slow, and risky at best.

As a whole, domestic oil and gas from fracking is beginning to look like an investment bubble.

As a whole, domestic oil and gas from fracking is beginning to look like an investment bubble. U.S. production of tight oil by fracking can probably only increase and postpone another global oil price spike for a few years. Even if the current fracking boom should somehow give us five more years, it doesn’t change the picture much. Driving will get less affordable because of fuel, and there will be a painfully short amount of time to prepare. Gasoline-powered cars are expensive and last for more than a decade, and the USA doesn’t have any good mobility alternative to serve its suburbs.

An oil glut for now

As we saw in Part 1, trying to convince the U.S. public that they might have a problem driving about three years from now is going to be a hard sell. Who is the driving public to believe, those who warn them about a problem a years from now, or their own eyes? This is especially true since anyone who fills up at the gas pump can see for themselves that gasoline has been getting a bit cheaper lately.

For now, oil and its products remain a buyer’s market. Here we see the Wall Street Journal telling us that the reason that gas prices are going down is because of a glut of gasoline.

A global glut of crude oil is the main driver behind the decline in gasoline prices. Relatively cheap oil has made it more profitable for refiners to produce gasoline and other fuels, and they have ramped up production to record levels. This boom in supplies has sent gasoline prices tumbling. Traders and other market observers expect the flow of both crude oil and gasoline to keep rising, likely exerting more downward pressure on prices.

We are now at the doorstep of globally peaking oil

When I say that Americans will probably have trouble driving in only three years, this means that I think another oil price shock causing widespread public driving anxiety is quite likely by then. It could be less than three years; James Howard Kunstler gives us two years for reasons similar to mine.

Wait until they discover that the shale oil producers have never made a buck producing shale oil, only on the sale of leases and real estate to “greater fools” and creaming off the froth of the complex junk financing deals behind their exertions. Expect that mirage to dissipate in the next 24 months, perhaps sooner if the price of oil keeps sinking toward the sub $90-a-barrel level, where there’s no economically rational reason to bother drilling and fracking.

Gasoline is cheap for now only because oil production is relatively constant and the oil must be sold at whatever price the global market can bear, even during a time of global deflation due to the lingering effect of the 2008 oil price shock.

The estimate of three more years of easily affordable driving is an educated guess, based on looking at the work of a number of expert forecasters and analysts who predict that the global oil market will run out of profitable U.S. fracking plays in about this time. After another oil price spike we’re back to a bad recession like 2009, but this time with even less of the oil needed to recover.

The price of oil has a complex and partly hidden effect on the economy.

The price of oil has a complex and partly hidden effect on the economy. Since cheap conventional oil globally peaked in 2005, the higher price of fuel has acted like a slowly increasing but hidden tax on almost everything sold, since almost everything sold has some rising oil price costs embedded in its sales price. People cut back on discretionary spending in order to pay more for gas, which sent those sectors into recession. A hidden oil tax tends in this way to cause the pervasive economic stagnation we now see.

A rapid oil price spike is a much more politically visible target than the general stagnation effect of high energy prices, since an oil price spike leads to higher fuel and food costs fairly quickly. These two impacts of high oil prices, one faster and one slower, generate different types of political and economic responses.

Without an economic recovery, which is itself unlikely without cheap oil, another gasoline price spike to even $4 dollars a gallon might now cause a broad and angry public demand for Congress to do something fast, a sort of a political tipping point. A return to gasoline rationing, like that used after the 1973 oil crisis, is one plausible way for politicians to try to ease the public’s driving pain.

Expert evidence for three more years of easily affordable driving

The estimate of three years of easily affordable driving depends primarily on estimating how long the current fracking boom, which is now holding down the global oil price, can be sustained. There seems to be almost a consensus, outside of government officialdom like the EIA, of maybe two or three more years.

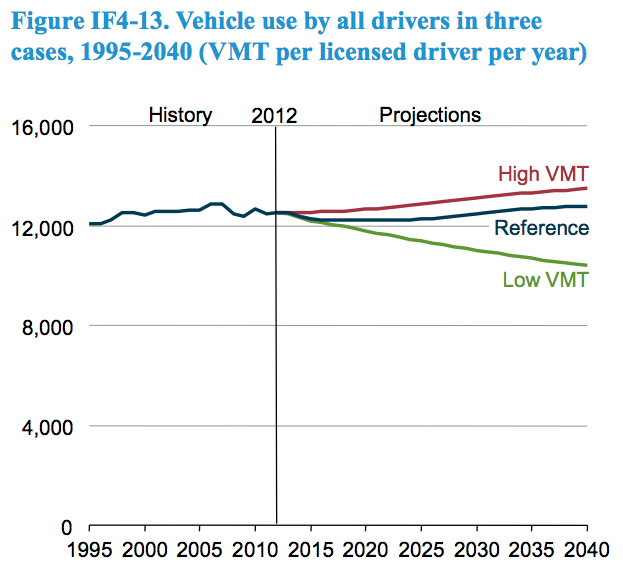

Figure 1 (above), taken from the EIA Annual Energy Outlook 2014, shows that their reference case expectation (business as usual) for future U.S. driving is totally flat for 2015-2025 (which actually means a decrease in driving per person). The EIA Low VMT (vehicle miles traveled) scenario shown indicates a very gradual and roughly 10% decrease in total driving 2015-2025 as the worst case scenario.

Post Carbon Institute fellow and author Richard Heinberg has written an exceptionally well-researched book, published in July 2013, titled Snake Oil: How Fracking’s False Promise of Plenty Imperils our Future.

In this interview, Heinberg reviews our energy situation; you can get a good idea where things stand just by listening to about the first 10 minutes. Following is a quote from Heinberg’s recent writing: “Why Peak Oil Refuses to Die. ”

Let’s start with the common assertion that oil supplies are sufficiently abundant so that a peak in production is many years or decades away. Everyone agrees that planet Earth still holds plenty of petroleum or petroleum-like resources: that’s the kernel of truth at the heart of most attempted peak-oil debunkery. However, extracting and delivering those resources at an affordable price is becoming a bigger challenge year by year. For the oil industry, costs of production have rocketed; they’re currently soaring at a rate of about 10 percent annually. Producers need very high oil prices to justify going after the resources that remain—tight oil from source rocks, Arctic oil, ultra-deepwater oil, and bitumen. But oil prices have already risen to the point where many users of petroleum just can’t afford to pay more. The US economy has a habit of responding to oil price hikes by swooning into recession, and during the shift from $20 per barrel oil to $100 per barrel oil (which occurred between 2002 and 2011), the economies of most industrialized countries began to shudder and stall. What would be their response to a sustained oil price of $150 or $200? We may never know: it remains to be seen whether the world can afford to pay what will be required for oil producers to continue wresting liquid hydrocarbons from the ground at current rates.

Heinberg’s shale oil book is partly based on the work of a top Canadian resource geologist, David Hughes, who did a study of tight oil and gas economics for the Post Carbon Institute, titled “Drill Baby Drill.” The report can be downloaded here. Basically what Hughes says is that there are only a few geographically large shale plays which contain within themselves much smaller sweet spots, those areas which are profitable when used to produce fairly high priced oil or gas. But these fracking wells tend to deplete rapidly, and the truly profitable sweet spots are being used up fast, implying that U.S. shale oil production will peak about 2017.

Hughes explained that more than 80 percent of the nation’s shale oil comes from just two plays, the Bakken field in North Dakota and Montana and the Eagle Ford in Texas. He estimates that production in those regions will recede back to 2012 levels in 2019. Overall production across the nation’s shale oil fields will peak in 2017.

Readers who want to review and keep abreast of the evidence should become familiar with the peak oil blogs.

Readers who want to review and keep abreast of the evidence should become familiar with the peak oil blogs. Ron Patterson posts on Peak oil barrel. Crude Oil Peak is another excellent source Yet another is Peak Oil News.

In this article — “US shale oil growth covers up production drop in rest-of-world” — we see charts that tell us that that an increase in U.S. shale oil production is now the one factor that has kept otherwise declining global oil production increasing. Tight oil has been effectively obscuring the pricing signals that peaking oil in the rest of the world would give, as global oil need, if not ability to buy, continues to rise.

Here is what a top Saudi geologist, now in private practice as a consultant, had to offer in an interview with ASPO-USA earlier this year (“Ex-Saudi Aramco geologist Dr Husseini predicts oil price spikes of USD 140 by 2016-17: graphs”)

Husseini: My base oil price forecast in 2012 dollars still ranges between $105 and $120/barrel Brent with a volatility floor of $ 95/barrel and more probable upward spiking to $140/barrel within 2016/2017.

Dr. Husseini didn’t say how he predicted the oil price spike, but Crude oil Peak analyst Matt Mushalik comments on the Husseini interview. The last graphic predicts that rising demand will meet the falling production predicted by Dr. Husseini about 2016, and concludes as follows:

We see that the intersection point is somewhere in 2016. What is more important than the precise year in which the next oil crunch may happen is the widening gap in the 2nd half of this decade.

Conclusion: Whether the world wants to follow the New Policies Scenario of the IEA WEO 2013 is another question altogether. It seems governments are rather on a current policies track which increases oil demand and therefore pressure on oil prices.

Here is a graphic that illustrates what might happen when fracking declines. See Figure 1. The red region representing tight oil is the only thing that has kept total world oil production from having already peaked. This is evidence that only a continuation or increase in the current level of U.S. tight oil production from shale can prevent another oil price spike followed by an economic bust.

The Medium Term Oil Market Report of the International Energy Agency (IEA, Paris), published in June 2014, contains a graph which implies that US crude production will start to peak in 2016. Few took notice although the world is continuously occupied with oil and energy related conflicts and wars in Ukraine, Libya and Iraq. So far, oil prices increased only shortly when fights flared up. Apparently oil markets are at ease while the US tight oil “revolution” is underway. But for how long?

The graph [Fig 1: US tight oil and crude oil in rest of world vs oil prices] shows that US tight (shale) oil sits on top of a bumpy crude production plateau in the rest of the world which clearly started in 2005 (average of 73.4 mb/d since Jan 2005). Despite increasing tight oil production oil prices did not go down but stayed at a level of around US$ 100 a barrel. We can safely say that without US tight oil – in May 2014 around 2.9 mb/d – the world would be in a deep oil crisis. People got accustomed to a higher oil consumption level which will be hard to come down from. Between 2005 and 2007, oil production declined by around 2 mb/d (supply shock) and oil prices doubled. That gives us an idea what will happen when tight oil starts to decline. So it is important to know when tight oil reaches its tipping point.

Another prediction that tight oil from fracking will top out in its domestic production in only about three years comes from the U.S. federal government, via the Energy Information Agency (EIA) and its periodic Outlook report.

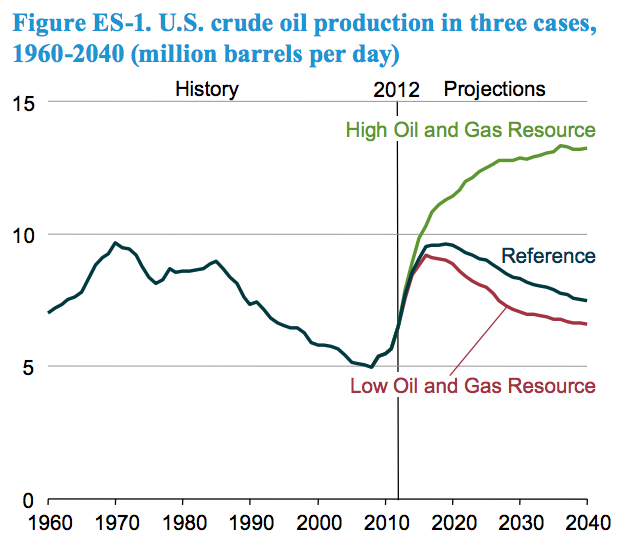

Figure 2 (above) is U.S. crude oil forecasts taken from the EIA Annual Energy Outlook 2014 and shows a sharp rise due to fracking of tight oil during 2012, leveling off about 2016, followed by a plateau extending a few years past 2020, and then a gradual decline. Contrast this with Laherrere’s prediction showing a domestic peak about 2017, followed by a fast decline, see Figure 4 below.

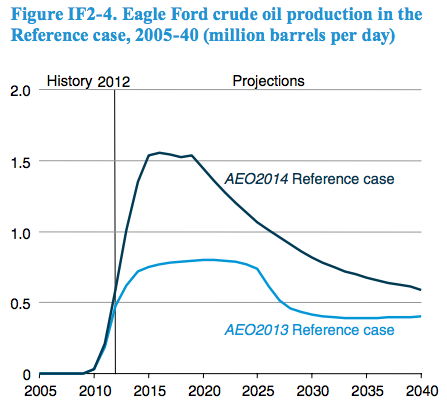

Figure 3 (above) shows the projected Eagle Ford tight oil output for 2013 and now 2014 from the EIA Annual Energy Outlook 2014.

See how much difference a year can make in the “reference case” or business as usual expectations, about doubling the expected future output. However if fracking expectations can double in a single year, how accurate is the EIA tight oil production model? How sensitive is the model to oil price? Why not show the model and also show the expected tight oil output for a high, medium, and low oil price? If our future driving affordability is tied to this oil output, we deserve good data transparency.

Here is how top oil analyst Tom Whipple of ASPO-USA reviewing the tight oil production situation recently put it.

The two major forecasting agencies, Washington’s EIA and Paris’ IEA, are both more pessimistic than is generally known for they both foresee US shale oil production leveling off as soon as 2016. The reason for this is that drillers will simply run out of new places to drill and frack new wells. While new techniques of extracting more oil from a well are possible, there is need to look closely at the costs of these techniques vs. the potential payoff.

The shale oil situation in Texas is somewhat different than in North Dakota, for there you have much better weather and two separate shale oil deposits. The recent growth in Texas’s shale oil production has been much smoother than in storm-prone North Dakota and has been increasing at about 44,000 b/d each month. So far as can be seen from the outside of the industry, production in both states will continue to grow for at least another year or two — but then we will be at 2016.

The government has never gotten around to publishing the assumptions that go into the forecast that U.S. shale oil production will stop growing circa 2016. The biggest difference between EIA/IEA and independent analysts is the government forecasters do not see a precipitous drop in shale oil production following the peak. Instead they see a period of flat production followed by a gentle decline stretching well into the next decade. Such a gentle end to the shale oil “bubble” can only assuage fears of a calamity. This projection on a gentle end to U.S. shale oil is at variance with outside forecasters who note that shale oil wells are pretty well gone in three years and simply do not see where the oil to maintain production levels will be coming from for another 10 or 15 years after the peak…

Independent analyses of U.S. shale oil generally come to the same conclusion that production will peak in the 2016-2017 time frame, but as noted above see a much faster decline than does the government.

Hydrofracturing for tight oil and gas is now about all that is left to maintain global oil production

Hydrofracturing for tight oil and gas is now about all that is left to maintain global oil production, as Art Berman points out in this interview: “Shale, the Last Oil and Gas Train”

Oil companies have to make a big deal about shale plays because that is all that is left in the world. Let’s face it: these are truly awful reservoir rocks and that is why we waited until all more attractive opportunities were exhausted before developing them. It is completely unreasonable to expect better performance from bad reservoirs than from better reservoirs. The majors have shown that they cannot replace reserves. They talk about return on capital employed (ROCE) these days instead of reserve replacement and production growth because there is nothing to talk about there. Shale plays are part of the ROCE story–shale wells can be drilled and brought on production fairly quickly and this masks or smoothes out the non-productive capital languishing in big projects around the world like Kashagan and Gorgon, which are going sideways whilst eating up billions of dollars. None of this is meant to be negative. I’m all for shale plays but let’s be honest about things, after all! Production from shale is not a revolution; it’s a retirement party. [emphasis mine]

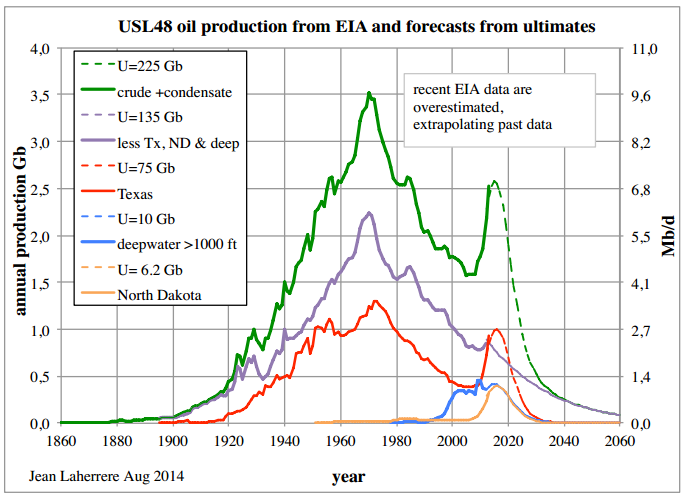

Finally, lets conclude this section with a peak shale oil prediction for 2016 made by one of the most skillful resource data analysts, Jean Laherrere, who along with Colin Campbell coauthored “The End of Cheap Oil” in Scientific American in 1998, when oil cost less than $20 a barrel. Scroll toward the end of the link and see a big green hump in a chart that represents the official EIA Outlook prediction of a peak in shale oil in 2017. Laherrere’s peak for shale oil is followed by a much steeper decline rate as can be seen in the subsequent chart.

As we see in Figure 4 (above), Laherrere predicts a very rapid drop in tight oil production after 2017, leading also to a fast decline in total oil from the lower 48 states, in contrast to the EIA.

As Laherrere says:

It seems that most oil companies are spending more than their revenues by increasing their debts. Countries can live for a long time with huge debt increase, not companies. They count on the stock market by delivering optimistic reports and keep drilling to avoid the production to decline. With shale oil or shale play, in contrary with conventional where wells are dry or producing, oil can be produced even for a while if not economical.

Such behavior explains why most peak forecasts are wrong. But the main question is about the slope of the decline after the peak. EIA forecast a LTO (light tight oil = shale oil) peak in 2017 it is not too far after my forecast, the big difference is the slow EIA LTO decline.

Why fuel prices probably won’t fall much more

Why won’t the price of driving, as affected by fuel cost, go down very much or for very long? The Saudis alone can produce about 10 million barrels of oil a day mostly for export. This gives the Saudis the ability, acting as one country with a centralized oil production policy, to put a floor under the global oil price simply by cutting back on their oil offered for export. Abundant Saudi oil exports remain vital to a world of commerce built with and quite dependent on affordable oil.

The Saudis lack the excess oil production capacity that they once had, so they cannot flood the market to lower the oil price.

The Saudis lack the excess oil production capacity that they once had, so they cannot flood the market to lower the oil price. However the Saudis still have the critical market power, through cutting production, to keep global crude oil prices from sinking.

“We are swimming in crude, and they [the Saudis] know that better than anyone because they are the biggest exporter,” Mike Wittner, the head of oil market research at Societe Generale in New York, said by phone Sept. 9. “History shows that the Saudis will just do what’s necessary.” … Saudi Arabia made the biggest contribution to OPEC’s production cuts in 2008 and 2009 as demand contracted amid the financial crisis. The group took almost 5 million barrels of daily output off the market, reviving prices from about $30 at the end of 2008 to almost $80 a year later.

At its current price, “Brent has traded since early July within the range of $95 to $110 described as ‘fair’ by Saudi Oil Minister Ali Al-Naimi at a meeting of the Organization of Petroleum Exporting Countries in June.”

The Saudis have an incentive to pump at or near their maximum capacity, but to cut back when the global price sinks below their favored price range, neither so high as to hurt the global economy, nor so low that it puts other higher cost oil producers, which together supply most of the world’s other oil, out of business.

Both Saudi and Iran recently warned that declines in crude prices will be short lived. It is an ominous sign for motorists in the UK who were hoping that recent declines in the cost of a gallon of petrol would be sustained.

The Saudi’s favorable price band is shrinking and may not even exist any more because global oil customers are getting poorer, even while oil producers, especially private oil investors outside the Middle East, are losing money by producing oil under increasingly costly and difficult circumstances.

A timeless pattern of periodic energy investment overshoot

The human effort required to obtain and channel the energy needed to build and maintain an economy is a key feature of all civilizations, which ultimately limits their complexity and type of economic organization, as Tainter has pointed out. For this reason, changes in the supply and cost of motive power, whether this is derived from oxen and slaves consuming grain or from diesel engines burning oil, can cause civilizations to rise and fall and to win or lose wars.

The oil industry has always been characterized by boom and bust investment cycles.

As a primary and vital source of such power, the oil industry has always been characterized by boom and bust investment cycles, a pattern of exuberant investment in production followed by ruinous periodic production gluts. Frenzied oil production in the giant East Texas field during the early depression years caused the oil price to fall as low as 13 cents a barrel. The Texas governor called out the Texas Rangers to halt and regulate excessive production, which was permanently damaging oil fields.

Later regulation from the Texas Railroad Commission established allowable oil production limits that effectively set world oil prices from the 1930s until the 1960s. This Texas regulation of private producers later served as the regulation model for OPEC, created to prevent ruinous price volatility in the unregulated global oil market.

In Part 1, we saw the federal data compiled by the EIA, which indicates that not only are the top 127 energy companies losing money on oil and gas, but that meanwhile most OPEC oil producing countries are also having trouble meeting their costs by selling oil to a depressed global market.

Deep water oil production in the Gulf of Mexico was expanding fairly rapidly until recently. Since deep water oil is very expensive and risky — and not very profitable — production by the private majors like Exxon, those who can afford $180 million for a deep water well, have been shifting back onshore with the advent of fracking, which is more predictable in outcome and might only cost $8 million per well. Nobody would be doing deep water drilling in the Gulf of Mexico if there were profitable places left to drill on dry land, but now even the deep water drilling has tapered off.

“Deepwater is providing lower returns and has shown no production growth while U.S. unconventionals have much higher returns (at least on paper), [and] enough scale of reserves to be of interest to the majors … so according to them, they will shift spending,” Wicklund noted.

With current economic uncertainty, investors don’t know what the price of oil will be a few years into the life of the well. Until about 2012, the global price of oil was rising nicely, comfortably over $100 a barrel, but over the last two years it has been almost flat and is now decreasing due to a stagnant or deflating global economy.

But oil producers are tied to the existing market price, for better or worse. The market demand for oil-based fuel can rise or fall much faster than the supply tends to change. A low rate of drilling sets the stage for a future price rise when the return of a tight market causes global oil prices to rise again.

Since fracking is what is has been holding U.S. driving costs down, it stands to reason that when this rapidly depleting oil source goes into decline, fuel prices will rise and we will be obliged to drive less.

Military events which could seriously interfere with driving in less than three years

There are looming but plausible threats to widely affordable American driving that are widely understood to exist but are nearly impossible to accurately predict in their severity and timing. Two major “black swan” events are first, an interruption in steady oil exports from the Middle East, and second, a swiftly developing global economic crisis which could affect the U.S. and global economies.

Our current effort to militarily contain the Sunni-based Islamic State in Iraq and deescalate regional conflict is plagued with uncertainties, if not impossibilities. Nobody can easily anticipate how military turmoil in the Sunni regions to the north might affect oil production from the Shiite dominated oil-producing regions of Iraq to the south, which are currently producing and exporting about 3 million barrels of oil a day.

Trying to use U.S. military power to keep the Middle East reliably producing its oil for export has become a daunting military juggling act.

There is much to go wrong in a conflict that could spill over into nearby Saudi Arabia, which is itself increasingly unstable. Trying to use U.S. military power to keep the Middle East reliably producing its oil for export has become a daunting military juggling act. The new Prime minister of Iraq tells us that all foreign troops will be unwelcome at the same time our generals tell us that the conflict cannot be won from the air.

In light of this situation, we might be better off using diplomacy rather than relying on military power to achieve our goals.

Economic events which could seriously interfere with driving in less than three years

Gasoline has gotten a little cheaper at the pump lately, headed toward $3 a gallon, which has the welcome effect of stimulating the U.S. economy by putting some extra dollars in the pockets of most drivers. But it doesn’t change the big picture much.

The USA remains in an economic crisis because of low growth, a dependence on easy money from the Fed, and an inability to revive the U.S. economy despite a massive level of quantitative easing.

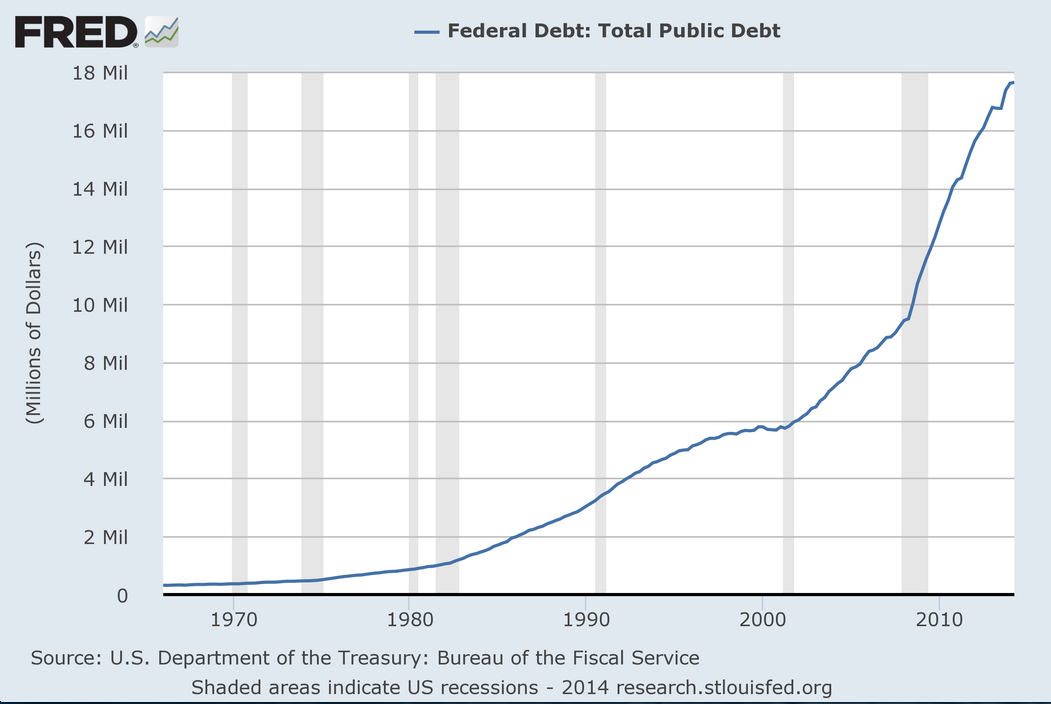

As we see from Figure 5 (above), a Saint Louis Federal Reserve Economic Data or FRED chart, there has been a lot of public debt going into keeping the economy stimulated, and keeping it from sinking into a deflationary spiral because of rising oil cost reducing the profitability of investments. This has not led to a broad recovery, so what happens when this growth in public debt slows or stops?

Figure 6, a chart of S&P 500 stocks, looks like a row of shark teeth rising, falling, and then rising higher. The first peak was due to the dotcom bubble, its crash, and then a recovery in the federal credit for the housing market boom until the housing bubble collapsed in 2008 about the same time as the the oil price bubble. Now the S&P index is rising yet higher again.

It is hard not to see that the easy credit and low interest rates are tied to the new public debt shown in Figure 5, and that this cash is seeking out stocks. It looks like the Fed’s quantitative easing is inflating stock prices, which are soaring, but that this cash is avoiding investment in the stagnating economy of high unemployment and minimum wage jobs familiar to those who don’t own stocks. The Nasdaq composite index looks even more peaky. Looking like an asset bubble in search of profitable investment in the self-promoting world of finance, rather than in the struggling hard times economy unable to keep growing without cheap oil. How high will the latest shark tooth get before it falls again?

It is is not widely understood that the great recession of 2008 was initiated when oil surged to $147 a barrel in mid-year, followed by a banking liquidity paralysis and a steep oil price collapse. This same event also tells us roughly what to expect when the current oil glut is succeeded by another oil price spike. Dr James Hamilton has done a lot of economic analysis that strongly links oil price rises to subsequent recessions.

The USA is slowly moving in the right direction, burning less oil and we are driving less than ever, but the easy progress has already been made. We still have to import roughly the same amount of oil that we produce domestically just to keep driving normally. There is essentially one big global oil market which has Americans bidding against the Chinese and everyone else for fuel, in the context of a shrinking supply of globally traded oil.

The Chinese economy now seems to be headed into its own growth slump.

The Chinese economy now seems to be headed into its own growth slump. For a decade or more, investments in many sorts of raw materials, including oil, have depended on strong Chinese demand that acted as an economic engine to maintain global trade and support rising commodity prices.

…In other words, we are now in a world in which the biggest economy, Europe, is about to enter a triple-dip recession, and the third largest standalone economy, China, is undergoing an economic standstill, and all hopes and prayers are that China will join the ECB in activating monetary easing once again. But yes, the Fed will not only conclude QE but will supposedly begin rising rates in just over two quarters. Good luck with that.

With a global economy depressed for years by the stress of about $100 a barrel oil prices, and with attempts to revive the US. economic growth ineffective, aside from what looks like a stock bubble, we could easily slip into a global deflationary spiral. It is not apparent that the global economy can grow at all without cheap oil. As a result, we have a world flush with dollars that have a very low velocity of circulation and a cautious deflationary spending psychology prevails.

Richard Heinberg’s book The End of Growth pointed out that, with the end of cheap oil, the global economy is likely to be incapable of real material growth, as opposed to financial sector growth. Good economists are starting to realize that the future doesn’t work very well without cheap oil.

Peak oil could be the catalyst for global collapse. Some see new fossil fuel sources like shale oil, tar sands and coal seam gas as saviours, but the issue is how fast these resources can be extracted, for how long, and at what cost. If they soak up too much capital to extract the fallout would be widespread.

Gail Tverberg in her excellent blog Our Finite World, thinks global deflation is happening now. (“Low Oil Prices: Sign of a Debt Bubble Collapse, Leading to the End of Oil Supply?”)

I would argue that falling commodity prices are bad news. It likely means that the debt bubble which has been holding up the world economy for a very long time — since World War II, at least — is failing to expand sufficiently. If the debt bubble collapses, we will be in huge difficulty…

Tom Whipple, who we saw comment earlier, points out that social and economic problems related to peak oil are already global, and are around us everywhere whether or not we are able to understand the connections.

If we step back and acknowledge that the shale oil phenomenon will be over in a couple of years and that oil production is dropping in the rest of the world, then we have to expect that the remainder of the peak oil story will play out shortly. The impact of shrinking global oil production, which has been on hold for nearly a decade, will appear. Prices will go much higher, this time with lowered expectations that more oil will be produced as prices go higher. The great recession, which has never really gone away for most, will return with renewed vigor and all that it implies…

All this is telling us that the peak oil crisis we have been watching for the last ten years has not gone away, but is turning out to be a more prolonged event than previous believed. Many do not believe that peak oil is really happening as they read daily of surging oil production and falling oil prices. Rarely do they hear that another shoe has yet to drop and that much worse in terms of oil shortages, higher prices and interrupted economic growth is just ahead. We are sitting in the eye of the peak oil crisis and few recognize it. Five years from now, it should be apparent to all.

Part 3 of ‘America: You’ve got three more years to drive normally!’

This is yet to come, and will examine what might happen when the tangle of problems that come with a faltering economy finally exceed our cultural capability for denial. Could an end to affordable driving create enough of a political shock to spur even our gridlocked congress to take decisive action? If so, what action? Gas rationing? Peak oil and global warming are two branches of the same denial syndrome, but of these two, driving affordability definitely has a shorter fuse.

Easy driving remains basic to American lifestyle and social identity. For now, Americans are still managing to drive nearly as much as they did a decade ago. But what happens in a few years, when gasoline prices keep going up as wages remain flat, when drivers bid for the same oil needed to heat homes in New England. Who gets the oil and who gets the blame? Will the loss of mainstream driving ability finally create a political tipping point that could lead us to broadly confront and accept natural limits to growth?

Read more articles by Roger Baker on The Rag Blog.

[Roger Baker is a long time transportation-oriented environmental activist, an amateur energy-oriented economist, an amateur scientist and science writer, and a founding member of and an advisor to the Association for the Study of Peak Oil-USA. He is active in the Green Party and the ACLU, and is a director of the Save Our Springs Alliance and the Save Barton Creek Association in Austin. Mostly he enjoys being an irreverent policy wonk and writing irreverent wonkish articles for The Rag Blog.]

Roger, you’ve been posting this ‘the world’s going to end tomorrow nonsense” now for 5 years. Go back and read some of it and please ask yourself… am I just the poor mans Paul Ehrlich? Well, don’t worry. Just like Ehrlich, I’m sure you’ll fiind that doomsday sellers always turn out… just like the neocons… harder to disprove than vampires.

I haven’t come back to this site for many years… and you have just reminded me why. I’m sure when I return 5 years from now, I’ll see another post warning me of impending doom penned by Roger Baker. Good luck.

Well, ‘doomers’ successfully predicted 11 of the last 3 recessions.

That any data points match their predictions at all, ever, is used as proof they are “right.”

But even a stopped clock is right twice a day.

why did you bother returning if you left before.Really if you are so sure about realistic analysis of our problems being wrong then your comment is unnecessary

Roger, your analysis and research on the oil end game are excellent — accessible and informative as always, especially where you put the fracking “cult of salvation” into perspective.

Of course, as the oil crunch gets closer, more and more people will be looking to shoot the messenger and to cling that much harder to their already-overworked denial.

The truth is that I have never previously, and am not now, posting what Sid Eschenbach calls “the world’s going to end tomorrow nonsense” or anything like that. That is simply an emotional burst of denial, based on no facts or numbers whatever. The things that I said about peak oil five years ago were true and based on evidence. In fact, the U.S. federal energy agency, the EIA, now admits that cheap ‘conventional oil’ did indeed peak in its global production in 2005.

The important issue, presuming that we are really engaging in intelligent discussion, is how much longer U.S. tight oil from fracking can delay a return of the kind of economically crippling fuel cost price spike that we saw in 2008, because peaking conventional oil was unable to meet global demand.

We can deny reality, but we cannot deny the consequences of denying reality.

I heard a Canadian scientist speak at UT years ago about peak oil. What you are saying makes sense to me. What can I do to prepare? Buy a motorcycle? Bicycle?

Presently, I am paying off all debts so that the money I earn will last as prices rise. I see the cost of living rising and my wag

Hi Joan,

I would suggest hanging out on Resilience.com website where they talk about the social side of dealing with a coming energy transition. Good material every day. A very well selected and nicely presented stream of articles.

Why is your curve of exploitation for the entire globe bell-shaped? What’s the magic about a half way point for a peak? Maybe exploitation just keeps rising until the resource gets completely tapped out, no “peak,” rather a cliff.

I know, I know, Energy Return on Energy Invested . But EROI for oil drilling changes depending on technology, which is still on the move, always developing, and not at all static.

Plus, you can use coal to extract the declining oil, even if the process itself is net energy negative. You would do so in order to get more flexible premium liquid fuel using the cheaper solid fuel. Also, as you know, you can refine coal itself to a liquid oil-like fuel.

Ah, but you only speak of a “peak” in conventional oil. But can’t you define “conventional” any way you want to prove whatever you want?

And how intellectually honest and rigorous is that? Actually a different “peak” happens at $20 a barrel cost, $50, $100, and so forth.

Much oil is “conventional” if that term is defined to mean “not tight” — it just sits under water or ice.

This is a manipulated discourse. You are playing with definitions instead of using the numbers, which actually show more drilling and extraction than ever.

Anonymous needs to do his or her homework. Conventional and unconventional oil are well known terms with conventional being the old wells that were drilled straight down until they hit oil that flowed by itself.

http://en.wikipedia.org/wiki/Unconventional_oil

Unconventional oil is generally all the other stuff that is hard to get.

Peak oil is really an economic peak. Oil peaks when it is no longer profitable to keep expanding production. The global economy like the current oil glut and fall in price can greatly affect the profit from drilling and thus the arrival of a peak.

If you use coal to extract other oil, there is less coal available to do other work. Are you paying attention to what you are saying at all? You are the fellow playing rhetorical games here.This has been dealt with before. You are confusing energy with technology. Energy is a latent condition preexisting in the universe. Technology enables us to utilize it.Oil,coal,natural gas, uranium-none of them were created by technology.

Wages flatline. But I do worry about transportation.

While conventional oil has peaked. Fracking is quite a ways further out than 2020. My brother is a petroleum engineer and brokers oil rights for the largest bank in the world. His estimate is that the fracking plays that are being drilled right now only represent about 20-40% of the explored reserves. The government estimates above only take into account a very conservative estimate of what is currently economically viable. When you look at what is happening in West Texas, they are drilling in 4-6 plays (layers). In Eagle Ford, they are only drilling in 1-2 relatively shallow plays. In each case there are several additional known (deeper) plays that haven’t been tapped, yet. The currently untapped shale in California is as large or larger than the Texas reserves. So peak “fracked” oil for the US is probably 20-30 years away, assuming no additional new discoveries. Known undrilled frackable reserves worldwide are 2X -5X what was available at the beginning of the frack boom in the US. Some are just in much more inaccessible territory, but given enough $ they can and will be accessed.

Who knows what other new inventions might push peak oil further out?

Also, the price of oil is currently highly inflated by the weakening of the US dollar by the Fed. If you look at natural gas prices, they translate to around $2.00-$2.50 as a gasoline equivalent. That’s probably the true price of gasoline if we didn’t have the Fed action.

Even if peak oil becomes a reality, the quickening decline of the cost of 100% electric vehicles and mainstreaming of natural gas engines takes much of the argument regarding both peak oil and emissions off the table.

Soon we will be able to have just as many or more cars on the road, but much lower emissions per car. And perhaps significantly lower total emissions as renewable energy sources are used to charge the 100% electric vehicles and additional alternative mobile energy (fuel cell) sources become available.

So the real argument for me regarding “the end of driving the car as you know it” is the infrastructure capacity. As right of ways begin to exceed their maximum car capacity, the only two ways to move more people are a) get a larger ROW or go away from the surface ROW; or b) change to a transportation mode that has more capacity.

For many places, getting the additional ROW is very hard politically and is often a significant financial hardship. Some roadways have grown so large it would seem that adding extra lanes have diminishing value. So it would seem that option “b” is the best answer to the capacity question. I think this is a much better argument for transit than trying to be a prognosticator on peak oil and global warming.

The claim:

“The currently untapped shale in California is as large or larger than the Texas reserves. So peak “fracked” oil for the US is probably 20-30 years away, assuming no additional new discoveries.”

The reality:

http://www.theguardian.com/environment/earth-insight/2014/may/22/two-thirds-write-down-us-shale-oil-gas-explodes-fracking-myth

“EIA officials told the Los Angeles Times that previous estimates of recoverable oil in the Monterey shale reserves in California of about 15.4 billion barrels were vastly overstated. The revised estimate, they said, will slash this amount by 96% to a puny 600 million barrels of oil.”

The one who blew the whistle on the bogus California fracking projections was the same David Hughes that I quoted in my article above. His report is here and came out before the feds finally admitted their fracking assumptions were vastly inflated:

http://www.postcarbon.org/reports/Drilling-California_FINAL.pdf

The sad truth is, according to the federal Energy Information Agency, seen at this link:

http://www.eia.gov/todayinenergy/detail.cfm?id=17311

Most energy companies are now losing money, and as we can see, these losses have grown enormously in the last two years. Companies have to sell their oil for what the market will bear. The global market is depressed now, and with slack demand coming from China and Europe, oil price can easily sink below its current cost of replacement, which has been rising as the price has been falling due to slack demand.

As for electric cars relieving the pressure on fossil fuels, the rich will always be able to buy Teslas, but if the fracking boom ends in three years as the experts I quoted predict, there is no way to increase affordable electric car production on this timescale.

As a followup comment in response to Mike Wong’s comments about the bright future of U.S. tight oil production, there is a parallel world of production through the hydraulic fracturing of shale to produce tight gas.

Lets look at that situation which is now a little more mature than the tight oil situation. Here David Hughes lays out the reality of tight gas production:

http://peak-oil.org/2014/04/eia-seriously-exaggerates-shale-gas-production-in-drilling-productivity-report/

Tight gas, like tight oil, has its own recent history of giving rise to finance investment bubbles, in their economics character and psychology resembling a gold rush.

As a leading example, take the case of Aubrey McClendon CEO of Chesapeake Energy, “America’s Most Reckless Billionaire”, as described in Heinberg’s Snake Oil book, pages 95-97.

http://www.forbes.com/sites/christopherhelman/2011/10/05/aubrey-mcclendon-chesapeake-billionaire-wildcatter-shale/

After the Chesapeake directors kicked Aubrey off the board for his financial indiscretions rivaling those of the Wolf of Wall Street, he resigned and set up shop at a new resource company just down the street in Oklahoma City, called American Energy Partners, which is now having problems of its own:

http://www.forbes.com/sites/christopherhelman/2014/02/27/man-on-fire-aubrey-mcclendon-raises-billions-to-finance-his-redemption/

“But the federal DOJ criminal probe continues. According to the DOJ, the maximum sentence under the Sherman Act for collusive acts like bid rigging is a $1 million fine and 10 years in prison. Here’s hoping McClendon can stay out of jail, redeem himself through American Energy, and even make it back onto the Forbes 400 list one of these days.”

Mousetrap dialogue box we have here.

Chesapeake Energy is also embroiled in other litigation:

“The issue is whether Chesapeake is giving Pennsylvanians short shrift on royalties for natural gas produced from their land. Leaseholders have accused the company of skimming royalties by deducting costs that should not be deducted…”

http://www.eenews.net/energywire/stories/1060005185

peak oil doesn’t need to become a reality.it is reality. There is only so much of any resource available at any time on a finite planet. The fact that we are currently “swimming” in oil(we are not)is predicated on the fact that we are at the all time peak of production. That recognizes that there is half of the resource available, and will decline gradually. Oil shale, is really more like coal than oil, and will only become available through huge is situ energy plants(nuclear power plants have been proposed for both tar sands and oil shale)or mining and removal to processing sites. It might happen but what are the actual consequences of these efforts?

Thank you for the in-depth analysis, copious links and references, and rebuttals that indicate you have “done your homework”. I appreciate it.

I think the 3-year estimate is a little too specific for me, but totally see how you came up with it based on the data available from various sources. And, glad you include others that say it could be two years – while others say five, or more. Three years also seems conveniently far enough out to ignore real change, but close enough to instill a bit of fear.

I think most of us are screwed if this comes to fruition as you describe; screwed in the sense that our lives will be totally up-ended. There will be mass layoffs, food shortages, possibly violence and political disruption. Stuff that Kunstler is good at describing. Even if you think you’re insulated because you have an electric car and solar panels (like I do), oil is a basic ingredient to make our economy function that is underestimated and would have far more of an impact than just not being able to drive our cars. Those who can survive with their neighbors to provide food and shelter outside the monetized economy will be ok. Others may take the “collapse” more personally or not have any way to provide in this way. Nevertheless, I take comfort in the fact that we could still be happy and provide for one another with dramatically reduced (say 90% less) energy expenditures, without political upheaval or significant loss to human life. We could. Not sure we will, but we could.

The only thing Roger gets wrong is an expectation

that people will actually read the material before

they counterpoint with their point of view.

Even the majors missed the potential of shale oil.

To this day none of the giant multinational oil

companies are more than marginally invested in

the recognized plays. It’s no wonder that the folks

studying peak oil in 2005 missed it too.

But what did they miss?

When the oil business is exploiting shale it is

horizontally drilling and fracturing the source rocks

for all the conventional oil accumulated in traps

over millions of years – the bottom of the barrel.

The recovery of this “tight” oil is very expensive

and resource intensive. The number of commercial

plays that will actually produce oil at a profit is

limited.

Shale gas is much more widely spread but we are

not now nor will soon be converting the personal

transportation fleet to natural gas. The infrastructure

to do this in the near term just isn’t there.

Many of the folks engaged with ASPO the

Association for the Study of Peak Oil have wildly

divergent points of view. The chair of the association

is Chairman of the Petroleum and Geosystems

Engineering Department at the University of

Texas. My perception is that he’s more the doomer

than Roger.

Most if not all recognize that the cornucopian

expectation that shale oil will deliver US energy

independence or even substantial oil much past

2020 is way overblown. That’s about 5 years out.

It could be as little as 3 years. Whatever, it’s not much

time to get our acts together – certainly not enough

time to replace roads with railroads in a timely

manner – or one that’s actually going to work for

families.

Waste of time to reply here only to have it disappear.

As you can see, Tim, nothing disappeared. We moderate comments for hate speech, personal attacks, and, especially, spam. But never based upon viewpoint. Sometimes there’s a short lag before a comment is approved.

The “peak” is beside the point.

We long ago passed the peak of horse-and-buggy production. We recently saw the peak of phone land line sets.

These events didn’t stop surface transportation and distance communication from expanding. In fact, it was because they WERE expanding that those particular old tech formats “peaked” in market penetration.

The peak in so-called “conventional” oil is completely contrived. If you can fuel your car, what does it matter where the gasoline comes from, whether ‘conventional’ or ‘unconventional’ ? If you can use electricity, you won’t need gasoline either.

Consider: three of the four biggest ‘conventional’ oil reserves in Iraq, Libya, and Iran. Combined, all as large or larger than Saudi Arabia, & less than half tapped. The reasons they are off-line have nothing to do with so-called ‘peak’ geology.

Ah, but the doomers no longer say that a peak is geologically “inevitable” — they redefine the term to mean politically and militarily challenging to get.

Consider: on Wikipedia’s “peak oil” page, “conventional’ as so defined is less than a third of total available stuff being counted there as ‘oil’ — bitumen, shale, undersea, heavier, lighter than “normal” or “traditional.”

Ah, but this stuff is more expensive to extract — at least for now. Like cars were compared to horse buggies, and cell phones compared to land lines.

But right now, the world price is going down, not up. But, oh, it means less profits for the oil companies because the cost of drilling is up and the demand isn’t there.

So, formerly increasing prices were cited by doomers as “proof” of a peak — now declining prices are.

With their ever-shifting set of rationales and definitions, the peak doom hypothesis can never be conclusively proved or disproved. Disaster is always around the corner, with no conceivable response available to avert it.

If you disagree with the peak tweakers, they accuse you of “denial” caused by hidden fear that the ‘oil party’ will be over.

No, it’s the opposite. They are denying that the abundant proof that their so-called peak is a mirage, because of hidden hopes that exogenous events will end the oil age.

The reasons to limit or halt oil production will be because we have something better available now, not because we are forced to by geology.

Everything else is contingent: the politics and social changes necessary to end climate destruction, Mid East militarism, and energy corporation monopolies, price gouging, and undue political influence. Geology will not do for us what we need to do for ourselves.

if it is a mirage, why do you bother replying as you do? There is no need. Things will be fine. What exactly is the point of peak horses. In all statistical analysis, there is a curve of maximums, and minimums This simply reflects the reality of living in a finite world. All the hard to access oil has been known for a long time. Nuclear explosions were proposed for extracting tar sands in the 1950s.The peak of any resource will always exist, because there is a finite amount of ANYTHING in this world. No amount of rhetoric can alter this reality

something better-otherwise known as substitution. Better is a relative term-its a value judgement,not a fact. People point out the various disadvantages of horses-all true. Cars-how many people have died, or been horribly mangled by automobiles since their invention?That’s only one small downside. That’s better than horse manure how exactly? Electric vehicles-not going to happen? What substitutes to real engineering problems do you propose besides clever wordplay