Thar She Blows: The Last Hurrah for the Banking System

By Mike Whitney / July 28, 2008

The Bush administration will be mailing out another batch of “stimulus” checks in the very near future. There’s no way around it. The Fed is in a pickle and can’t lower interest rates for fear that food and energy prices will shoot to stratosphere. At the same time, the economy is shrinking faster than anyone thought possible with no sign of a rebound. That leaves stimulus checks as the only way to “prime the pump” and keep consumer spending chugging along. Otherwise business activity will slow to a crawl and the economy will tank. There’s no other choice.

The daily barrage of bad news is really starting to get on people’s nerves. Most of the TV chatterboxes have already cut-out the cheery stock market predictions and no one is praising the “impressive powers of the free market” anymore. They know things are bad, real bad. A pervasive sense of gloom has crept into the television studios just like it has into the stock exchanges and the luxury penthouses on Manhattan’s West End. That same sense of foreboding is creeping like a noxious cloud to every town and city across the country. Everyone is cutting back on non-essentials and trimming the fat from the family budget. The days of extravagant impulse-spending at the mall are over. So are the “big ticket” purchases and the “go-for-broke” trips to Europe. Consumer confidence is at historic lows, disposal income is a thing of the past, and all the credit cards are at their limit. The country is drowning in red ink.

Something has gone terribly wrong with the economy, but no one knows what it is? In the last three months bank credit has shrunk faster than any time since 1948. The banks aren’t lending and people aren’t borrowing; that’s a lethal combo. When credit-creation slows, the economy falters, unemployment rises and the misery index soars. That’s why Bush will have to mail out more stimulus checks whether he wants to or not; his back is against the wall. He’ll try to make it look like the economy is still breathing on its own and just needs a spell on the respirator before resuming its normal activities. But Bush is wrong; we’ve reached Peak credit and the blood-transfusions won’t work anymore. The vital signs have shut down and rigamortis is already setting in. Our goose is cooked.

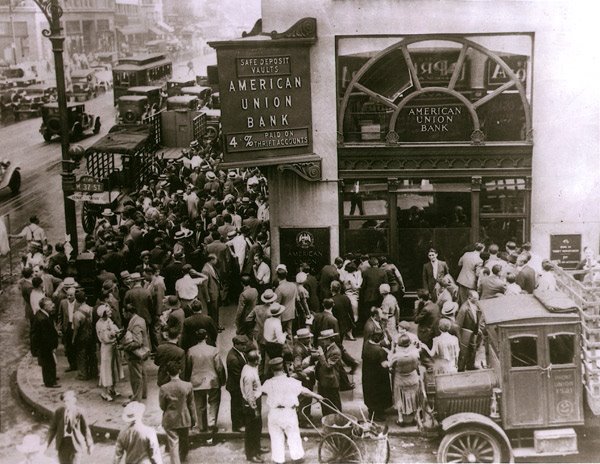

MORE BANK RUNS

On Friday, after the market had closed, the FDIC shut down two more banks, First Heritage Bank and First National Bank. Two weeks earlier, regulators seized Indymac Bancorp following a run by depositors. The FDIC now operates like a stealth paramilitary unit, deploying its shock troops on the weekends to do their dirty work out of the public eye and at times when it will least effect the stock market. The reasons for this are obvious; there’s only one thing the government hates more than seeing flag-draped coffins on the evening news, and that’s seeing long lines of frantic soccer moms and blue-collar working guys waiting impatiently to get what’s left of their savings out of their now-deceased bank. After all, flag-draped coffins merely indicate that we’re losing a war, but lines at the bank prove that the system is broken. And the system is broken, that’s why people are depressed and confidence is waning.

Banks-runs are a shock to the collective psyche; they demonstrate that the stewards of the system are imcompetent and have made a mess of things. When depositors see a bank run they realize that their hard-earned money is not safe. That’s why they get edgy and cut back on their spending. When their confidence wanes, it extends to the whole system. Suddenly they start questioning everything they once took for granted. They become skeptical of the institutions which, just days earlier, seemed rock-solid. That’s why bankers surround themselves with marble columns, vaulted ceilings and lofty-sounding titles; to maintain the illusion of security while masking the truth, that fractional banking is the biggest scam in history. It relies on the “greater fools” theory which assumes that bankers can be trusted to only create credit when it is backed by sufficient capital. But it is not true. The banks have put us all at risk.

Bank runs are a direct hit on the foundation of the free market system. Unchecked, the tremors can ripple through the entire society and trigger violent political upheaval, even revolution. The public may not grasp their significance, but everyone in Washington is paying attention. They take it seriously, very seriously. It is a sign that the system is disintegrating and it may be irreversible.

SABER-RATTLING AT THE FDIC

An article in the San Francisco Business Times said that the FDIC is worried about the reporting on Internet blogs. They’d rather keep banking system’s troubles out of the news. The publicity just further undermines the publics confidence and spreads fear. Sheila Bair, chairman of the Federal Deposit Insurance Corp., summed it up like this after the run on Indymac:

“The blogs were a bit out of control. We’re very mindful of the media coverage and blogs in controlling misinformation. All I can say is were going to continue to stay on top of it. The misinformation that came out over the weekend fed a lot of depositors’ fears.”

Is that a threat? The cure for a failed banking system is adequate capital and prudent oversight not threats to critics of the system. That’s balderdash. Commissar Blair apparently believes that bloggers should be treated the same way as journalists in Iraq, who, if they veer ever so slightly from the Pentagon’s “the surge is a great triumph” script, find themselves on the smoky end of an M-16 at some unmarked checkpoint outside Baquba.

If Blair wants people to take her seriously, she should stop the paramilitary-type mothballing operations to shut down banks and tell the American people the truth about what is going on. The banking system is busted; Blair knows that as well as anyone. Now its time for someone to accept the mantle of leadership, step up to the microphone and tell the public what they really need to know:

“My fellow citizens, we are embroiled in the greatest financial crisis our nation has ever faced and we will have to take emergency action to keep the entire system from melting down.”

How hard is that? But it won’t happen, because everyone in the administration has an aversion to telling the truth; it’s like the Devil and Holy Water. Besides, its easier to blame the bloggers, that harmless subspecies that spend long hours pecking away at their keyboards in their windowless 5′ by 7′ hovels.

Bloggers aren’t the problem; the problem is a system that’s collapsing from decades of abusive credit expansion creation and insufficient capital. Now everyone is going to pay for the excesses of the few.

As the bank-runs increase, the FDIC will be forced to admit the truth, that they don’t have the resources to deal with a problem this big. Currently, the FDIC has only $53 billion in reserves to guarantee $4 trillion in total bank deposits. The entire system has a mere $267 billion cash in the vaults. What a shabby way to run a banking system. Where’s the money going to come from when depositors start withdrawing their savings? How will the FDIC deal with the ongoing deleveraging in the market which is forcing more and more investors move into cash?

No one knows. All we get is more prevaricating; more smoke and mirrors, Bush assures us that “Our capital markets are functioning efficiently and effectively.” Nonsense. The markets are cratering and the banks are toast. A blind man can see it. The FDIC is listing and Blair knows it. Bush needs to cut the gibberish and tell the American people the truth so they can prepare for the hard times ahead.

P.T. PAULSON: “The the banking system is sound… This is a very manageable situation.”

Last Sunday, sought Treasury Secretary Henry Paulson tried to reassure the public that the banking system is sound, while bracing people for more trouble ahead:

“I think it’s going to be months that we’re working our way through this period — clearly months. But again, it’s a safe banking system, a sound banking system. Our regulators are on top of it. This is a very manageable situation.”

Paulson is like a broken record. Everything is always hunky-dory. He is the consummate Wall Street investment sharpie; a bright guy who could charm a hungry dog off a meat-wagon. But when it comes to telling the truth; forget about it. You’d be better off listening to Bush, which isn’t saying much. The banking system is not sound nor is it well capitalized. It is a corpse that’s been propped up in the office hallway next to the water-cooler so that everyone who passes bye gets a stifling whiff of the decaying flesh. Still, the charade goes on. Still the lies persist.

If the rate of bank closures continues at the present pace, by the middle of 2009 their will be restrictions on withdrawals. Even now, if you go to your bank and try to withdraw $9,000 or $10,000, it sends waves of panic through the entire building like a 5-alarm fire that quickly engulfs the main exits. It’s crazy. Tellers go scampering around helter-skelter, and bank managers suddenly appear at the window grimacing in pain and wringing the sweat from their brows.

“Did you say $10,000, sir?” which is usually followed by low moaning sounds and heavy wheezing.

Journalist Bill Sardi summed it up nicely in an article last week on lewrockwell.com titled “Could Your Bail Fail?”:

“The banking industry is walking on pins and needles, hoping the bad news doesn’t become a self-fulfilling prophecy that drives bank depositors to demand withdrawal of funds en masse…….. There is a high likelihood the American banking system will fail, and you will likely be the last to know. The more panicked you get, and withdraw funds, the worse the implosion. In an effort to avert runs on the banks, will the news media delay informing the public of the current dire situation, which appears to be an inevitable system-wide banking collapse?

What to do?

So, while your bank still has money and can process your checks, it may be time to pay down debts, pay quarterly taxes and mortgage payments in advance, and think of having money outside of banks (gold, foreign currencies), etc., before your money is inaccessible or even evaporates! Don’t think all your investments outside of banks are immune from all this turmoil. For example, money market mutual funds, where Americans have invested $3 trillion, are not covered by FDIC insurance (however, money market accounts offered by banks are covered). Recent losses in some of these money market mutual funds have caused some companies to rush to plug the losses. For example, Legg Mason Inc. and SunTrust Banks Inc., recently pumped $1.4 billion each into its money market funds. Bank of America Corp. has injected $600 million.

As for your checking and savings accounts, recognize you may have five different accounts in the same bank, but the FDIC only insures individuals, not each account, up to $100,000. Putting your money in different accounts in the same bank does not necessarily provide better insurance for your deposits. (Bill Sardi, “Could Your Bail Fail?”, lewrockwell.com)

Good advice, but if the whole system blows; we’re all in trouble. It’s probably wise to have a back-up plan; like plenty of ammo and a couple hundred pounds of seed potatoes. It could get hairy.

FANNIE BAILOUT: “If they dumped these securities on the market today, their value would go straight to 0.”

Most people are unaware of the fact that the new Fannie Mae and Freddie Mac bailout package that was passed into law on Saturday, provides Paulson with $300 billion of taxpayer dollars to shore up the faltering mortgage behemoths. In order to accomplish this, the congress increased the national debt by a whopping $800 billion sending it over the $10 trillion mark for the first time in history. Naturally the congress buried this little tidbit of information deep in the 600 pages of legislation. It’s clear that the administration is lying about Fannie and Freddie. They’ll need much more than the $25 billion infusion that Paulson is predicting. That’s why the national debt is ballooning. This is the biggest boondoggle of all time and it’s spearheaded by the “dueling windbags”, Chris Dodd and Barney Frank; both Democrats. Dodd’s lengthly oratory on the floor of the House on Friday nearly earned him a citation from the EPA for releasing massive levels of toxic gas into the jet-stream and accelerating the rate of global warming.

So it’s not just the Fed and the Treasury that are ruining the system; the politicos are busy bankrupting the country, too. In fact, the Fannie bailout could quite possibly be the last straw.

It now looks like Obama has been anointed by Wall Street (who are his biggest contributors) to revive the Resolution Trust Corporation (RTC)–a morgue for dead banks—so that the investment giants can off-load hundreds of billions in bad paper in one fell swoop and purge the system. That will be the big “post election” surprise; another bone for investment giants.

The path ahead has never looked so uncertain. Still, niether Paulson nor Bernanke seem at all upset by the riskiness of their strategy or by the fact that the nation’s economic future has been reduced to a crap-shoot. The Fed has already spent more than $300 billion to prop up the teetering banking system in the last year alone, plus another $29 (that was never approved by congress) to buy the toxic bonds from Bear Stearns in the JP Morgan acquisition. Now, the Treasury has been authorized by congress to buy an “unlimited amount” of Fannie and Freddie shares at their own discretion. They are presently exchanging Fannie and Freddie securities for US Treasurys, which means that the dollar is now backed by dodgy mortgage-backed sludge for which there is no market. According to Rep Ron Paul, “This is the asset (MBS) which now backs up our currency. An asset that no one else wants. If they were to dump these securities on the market today, the value of these stocks would go straight to 0. But that is literally the asset that is behind our currency. It is a very serious situation.”

None of congress’s back-room maneuvering has anything to do with “providing a lifeline for the struggling homeowner”, as Senator Dodd claims. That’s all bunkum. The homeowner won’t get a lick of help from this bill. Its just another handout for the brokerage fraternity. The country is putting its AAA credit rating on the line for same clatter of carpetbaggers who created the mammoth equity bubble in the first place. Now they are being rewarded for their criminal conduct. Also, Bloomberg News notes that, “Sensible people are starting to question whether the U.S. can hang on to its AAA credit rating. The prospect of an extra $5 trillion or thereabouts leaking onto the U.S. government’s tab from Fannie Mae and Freddie Mac has spooked investors.”

America’s AAA rating will vanish in a year. It should be zero anyway. No one really believes the US will repay its debts. The US bond market is just a glitzy imitation of casino roulette only the odds are considerably worse.

Our political leaders have engineered this whole farce and are now speeding up the process by savaging the dollar. How long before foreign creditors see through this ruse and dump their dollar-backed assets on the open market? The hoax can’t go on forever.

Of course, some market analysts think the banking system will make it through this rough patch, even though it is likely to take a real pasting. Economics guru, Gary North, for example, expects a slightly different outcome which he details in his latest article on Lew Rockwell’s web site “Ben Bernanke’s Hush Money”:

“There is an enormous difference – a literally life-and-death difference – between individual bank failures and a systemic banking failure. I do NOT believe we are facing a systemic banking failure. But we are facing more individual bank failures…

Beginning in December 2007, the Federal Reserve System has sold Treasury debt whenever it has increased its purchase of questionable assets that it has bought from banks and large financial institutions. It has unloaded about 40% of its holdings of liquid Treasury debt. This has kept it from inflating the money supply at a dramatic rate. At some point, it will run out of Treasury debt to sell to the general public in order to offset the increase of its purchase of questionable assets held by the financial system. At that point, the great inflation will begin. This could be a year away. This could be a month away. All we know is this: when the Federal Reserve system runs out of Treasury debt to sell, its purchase of all assets will be inflationary. The banking system as a whole is protected. What is not protected is the purchasing power of the dollar.” (“Ben Bernanke’s Hush Money”, Gary North, lewrockwell.com)

North makes a good point; when the Fed runs out of US Treasuries, they’ll have to rev-up the printing presses and monetize the debt. That’ll be doomsday for the dollar. When foreign central banks see the greenbacks a-gushing like the blood from a harpooned whale; they’ll have to sell off their dollar stockpiles and take the loss. That will trigger a period of hyper-inflation in the US. Everyone will pay for the excesses of the few.

The whole system has been rejiggered to serve the needs of a few greedy bankers on top of the food chain. They could care less whether the whole country blows up or not as long as they get their slice of the pie. That’s all that matters. Congress is just as bad. They abdicated their most important responsibility by giving Paulson the authority to take whatever money he needs to do whatever he wants. If that’s their attitude, then what do we need congress for? Let’s just board up the House of Representatives and send them all home. It would be a lot cheaper.

The truth is, the big money guys have taken a wrecking-ball to the financial system and have now moved on to the real economy. By the time their done, we’ll all be picking through the wreckage just to feed our families.

Source / Information Clearing House