Click on graphs below to enlarge.

The cost of wind, the price of wind, the value of wind

By Jerome Guillet and edited by Paul Spencer / June 2009

I’d like to try to clear some of the confusion that surrounds the economics of wind-based power generation systems, since opponents often try to use cherry-picked economic data to dismiss wind-power. As I noted recently, even the basic economics of energy markets are often willfully misunderstood by commentators, so it’s worth going into more detail through concepts like levelised cost and marginal cost, in order to identify how the different impacts on electricity wholesale prices (which may or may not be reflected in retail prices) arise via different electricity-production systems.

Equally important, these different production systems present different externalities, or cost impacts that are not typically registered in standard financial accounting. Value of a power-generation source may also include other items that are harder to account in purely monetary terms (and/or whose very value may be disputed), such as the long term risk of depletion of the fuel, or energy security issues, such as dependency on unstable and/or unfriendly foreign countries or on vulnerable infrastructure. Depending on which concept you favor, your preferred energy policies will be rather different.

The usual disclosure: my job is to finance, among other energy projects, wind farms. My earlier articles on wind power can all be found here.

Costs

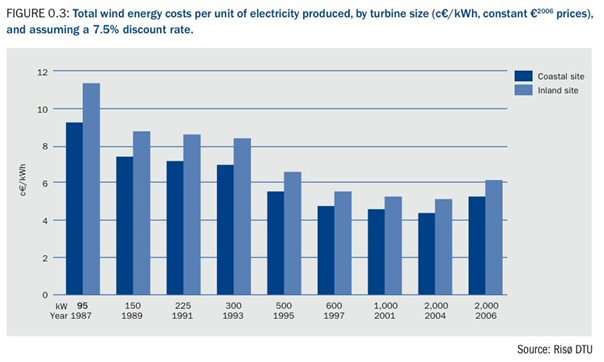

The cost of wind is, simply enough, what you actually need to spend to generate the electricity. The graph below shows how these costs have changed over the past decade: a long, slow decline as technology improved, followed, over the past 3 years, by an increase as the cost of commodities (in the case of wind, mainly steel) increased, and as strong demand for turbines allowed the manufacturers (or their subcontractors) to push up their prices:

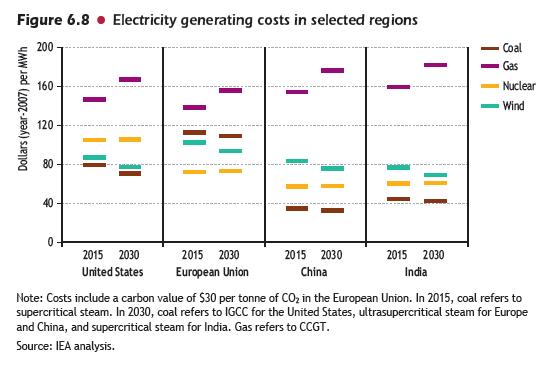

The most recent Energy Outlook by the International Energy Agency suggests that wind power currently costs €60/$80 per MWh, which makes it competitive with the major electricity-generation systems’ (nuclear, coal, gas) costs:

In the case of wind, it is important to note that most of the costs are upfront. I.e., you spend money to manufacture and then to install the wind turbines (and to build the transmission line to connect to the grid, if necessary). Once this is done, there are very few other actual costs: some maintenance and some spare parts now and then.

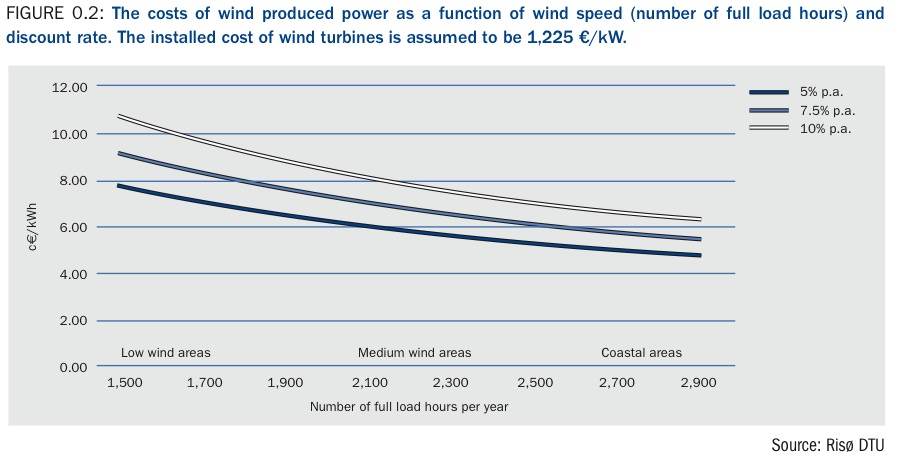

This means that the levelised cost of wind (i.e., the average cost over the long run, when initial investment costs are spread out over the useful life of the wind turbines) is going to be highly dependent on the discount rate (the estimated amortization used to spread the initial cost of investment over each MWh – megawatt-hour – of production over the useful life of the wind turbine. This ‘useful life’ is determined both in terms of duration, and of the interest rate applied.) The graph below shows the sensitivity of the cost of wind depending on the discount rate used (over 20 years):

The discount rate is the cost of capital applied to the project, it will depend on whether you can find credit (whose price can depend on your credit rating), or whether you need to provide equity (which is usually more expensive). Altogether, this means that most of the revenue generated by a wind farm at any point during its lifespan will go to repay the initial investment rather than to actual short term production costs; moving the discount rate from 5% to 10% increases levelised costs by approximately 40% (whereas for a gas project, it would typically be less than 20%).

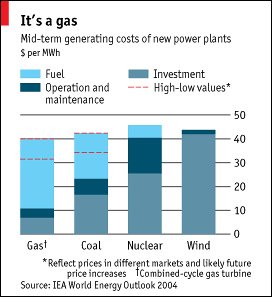

As a consequence, the marginal cost of wind is essentially zero; i.e., at a given point in time, it costs you nothing to produce an extra MWh (all you need is more wind). In contrast, the marginal cost of a gas-fired plant is going to be significant, as each new kWh requires some fuel input: this marginal cost is very closely related to the price of the supply of the volume of gas needed to produce that additional MWh.

The cost structure of wind and gas-fired power plants are completely different, as the graph above (from the Economist) shows: the Wind column includes mostly finance costs, the Gas column shows mostly fuel costs (with nuclear closer to the economics of wind, and coal closer to the economics of gas).

It is worth emphasizing that “letting the markets decide” is NOT a technology-neutral choice when it comes to investment in power generation: public funding (such as can be available to State-owned or municipal utilities) is cheaper than commercial fund of investment: given that different technologies have different sensitivities to the discount rate, preferring “market” solutions will inevitably favor fuel-burning technologies, while public investment would tilt more towards capital-intensive technologies like wind and nuclear.

This also means that, once the investment is made, the cost of wind is essentially fixed, while that of gas-fired electricity is going to be very variable, depending on the cost of the fuel. The good news for wind is that its cost is extremely predictable; the bad news is that it’s not flexible at all, and cannot adjust to electricity price variations.

Or, more precisely, wind producers take the risk that prices may be lower than their fixed cost at any given time. Given that, as a zero-marginal-cost producer, the marginal cash flow is always better when producing than not; wind is fundamentally a “price-taker”. I.e., the decision to produce will not depend on the price of fuel; however, the ability to repay the initial debt will depend on the level of the price of electricity. If prices are too low for too long, the wind farm may go bankrupt. Meanwhile, gas producers take a risk at any time on the relative position of the prices of gas and of electricity (what the industry calls the “spark spread“). This is a short term risk: gas-fired plants have the technical ability to choose to not produce (subject to relatively minor technical constraints) at any given time. They can thus avoid any cash flow losses, and the very fact that they shut down will influence both the gas price (by lowering demand) and the electricity price (by reducing supply). In fact, as we’ll see in a minute, electricity prices are directly driven, most of the time, by gas prices. Thus gas-fired plants are “price-makers”, and their costs drive electricity prices.

This suggests, once again, that selecting market mechanisms to set electricity prices (rather than regulating them) is, again, not technology neutral: here as well, deregulated markets are structurally more favorable to fossil fuel-based generation sources than publicly-regulated price environments.

At this point, the conclusions on the cost of wind power (ignoring externalities, including network issues which I discuss below) are that they seem to be similar in scale to those of traditional power sources (nukes, gas, coal), but that they have a very different relationship to prices.

So let’s talk about prices.

Prices

There are two aspects here: the price received by wind producers, and the price paid by buyers of electrical power.

The price of wind energy is what wind energy producers get for their production. It may, or may not, be related to the cost of the generation, but you’d expect the price to be higher than the cost, otherwise investment would not happen. But the question is whether the price needs to be higher all the time, or just on average, and, if so, for what duration.

Given that wind has fixed costs, all that a wind producer requires is a selling price which is slightly above its long term costs. That makes investment in wind profitable and actually rather safe. The problem, as we’ve seen, is that wind is a price-taker; and, unless producers are able to find long term power purchase agreements (PPAs) with electricity consumers at prices that permit debt service, it is subject to the vagaries of market prices. When your main burden is to repay your debt, and you don’t have enough cash for too long (because prices are below your cost for that period), your creditor can foreclose on the investment debt. This is true even though you can generate a lot of cash (remember that wind is a zero-marginal-cost producer and can generate income, whatever the market price is) – which means that a bankrupt wind farm will always be a good business to take over; it’s just that it may not be a good business in which to invest, if prices are too volatile…

Therefore, it is not surprising that the most effective system to support the development of wind power has been so-called feed-in tariffs whereby the wind producers get a guaranteed, fixed price over a long duration (typically 15 to 20 years) at a level set high enough to cover costs. The fixed price is paid by the utility that’s responsible for electricity distribution in the region where the wind farm is located, and it is allowed by the regulator to pass on the cost of that tariff (the difference between the fixed rate and the wholesale market price) to ratepayers. It’s simple to design, it’s effective and, as we’ll see, it’s actually also the cheapest way to promote wind. Other mechanisms include quotas which can be traded (that’s what green certificates or renewable portfolio standards are) or direct subsidies, usually via tax mechanisms. Apart from tax benefits, which are borne by taxpayers, all other schemes impose a cost surcharge on electricity consumers (although, as we’ll see below, in the case of feed-in tariffs, that surcharge may not exist in reality).

But there’s an even trickier aspect to wind and electricity prices: in market environments, under marginal cost rules, the price for electricity is determined by the most expensive producers needed at that time to fulfill demand. Demand is, apart from some industrial use, not price sensitive in the very short term, and is almost fixed (people switching lights and A/C on, etc…), so supply has to adapt, and the price of the last producers that needs to be switched on will determine the price for everybody else.

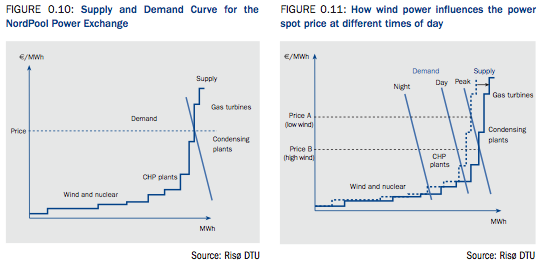

If you look at the above graph, you see a typical ‘dispatch curve’, i.e., the line representing generation capacity, ranked by price. Hydro is usually the cheapest (on the left), followed by nuclear and/or coal, and then by gas-fired plants and CHP (co-generation of heat and power) plants, followed to the far right by peaker plants, usually gas- or oil-fired.

The demand curve is shown by the nearly vertical lines on the right graph. The intersection of the two curves gives the price. As is logical, nighttime demand is lower and requires a lower price than normal daytime prices, which are, of course, less than peak demand which requires expensive (“peaker”) power generators to be switched on.

The righthand graph shows what happens when wind comes into the picture: as a very low marginal-cost generator, it is added to the dispatch curve on the left, and pushes out all other generators, to the extent that it is available at that time. By injecting “cheap” power into the system, it lowers prices. The impact on prices is low at night, but can become significant during the day and very significant at peak times (subject, once again, to actual availability of wind at that time).

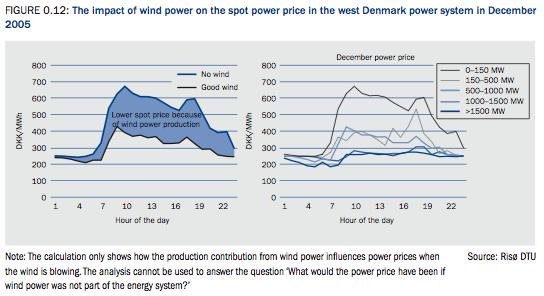

As the graph above suggests, the impact on price of significant wind injections is high throughout the day and is highest at times of high demand. When there’s a lot of wind, you end up with prices that get flattened to the price of base load (the marginal cost of nukes or coal) at which point wind no longer has any downward influence on price.

The consequence of this is that the more wind you have into the system, the lower the price for electricity. With gas, it’s the opposite: the more gas you need, the higher the price will be (in the short term, because you need more expensive plants to be turned on; in the long run, because you push the demand for gas up, which raises the price of gas, and, therefore, the price of electricity from gas-burning plants).

In fact, if you get to a significant share of wind in a system that uses market prices, you get to a point where wind drives prices down to levels where wind power loses money all the time! (That may sound impossible, but it does happen because the difference between the lowered marginal cost and the higher long term cost of the capital investment is so big).

There are two lessons here:

• wind power has a strongly positive effect for consumers, by driving prices down during the day.

• it is difficult for wind power generators to make money under market mechanisms unless wind penetration remains very low. This means that if wind is seen as a desirable power-generating system, ways need to be found to ensure that the revenues that wind generators actually get for electricity are not driven by the market prices that they make possible.

That’s actually the point of feed-in tariffs, which provide stable, predictable revenue to wind producers, ensuring that their maximum production is injected into the system at all times, which influences market prices by making supply of more expensive producers unnecessary. And these tariffs make sense for consumers. The higher fixed price is added to the bill for the buyers of electricity, but as that bill is lower than it would have otherwise been, the actual cost is much lower than it appears. As I’ve noted in earlier diaries, studies in Germany, Denmark and Spain prove that the net cost of feed-in tariffs in these countries actually has a negative effect on prices. That is, the fixed cost imposed on consumers ends up reducing their bills!

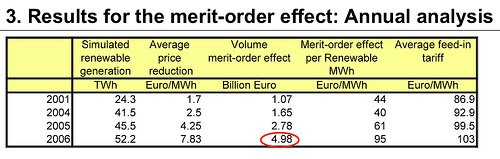

The table above indicates that renewable energy (mostly wind, plus some solar) injections into the German electricity system caused, on average over the year, total price for electrical power to be reduced by about 8 euros/MWh – about 15%. That translated into savings of 5 billion euros over the year for electricity buyers (utilities and other wholesale consumers), or 95 EUR/MWh for just the renewable energy component. With a feed-in tariff for all renewables of approximately 103 EUR/MWh (the wind tariff component is around 85 EUR/MWh), the net cost for the renewable sector is thus under 10 EUR/MWh, compared to an average wholesale price of 40-50 EUR/MWh. Thanks to the feed-in tariff, a wind MWH costs one fifth of a coal MWh!

In other words, by guaranteeing a high price to wind generators, you ensure that they are around to bring prices down. And that trick can only work with low marginal-cost producers (e.g., wind-based). It cannot work with any fuel-based generator, which would need to pay for fuel in any case. Such an arrangement might end up requiring a higher price than the guaranteed level to break even, if fuel prices increase – a likely event if such a scheme was implemented, because it would encourage investment in such plants, increasing demand for the fuel.

So we get a glimpse of the fact that there is value in wind power for consumers which is not reflected directly through current electricity prices, and is only remotely related to the actual cost of wind.

Value / externalities

This brings us to our last point: The “value” of wind power should/must include the other impacts of wind power within the economic system that are not captured by monetary mechanisms. This is what economists call externalities; i.e., the impact of economic behavior or decisions which are not reflected in the costs or prices of the economic entity taking the decision. Pollution is a typical externality, as is the impact on the distribution grid of bringing in a new energy producer.

Regulation is meant to put a price on these ‘external’ items, in order to reflect the “true cost” of a given economic action. Among the externalities that we need to discuss here are the intermittency of wind; carbon emissions (which, in this case, is an existing, improperly-priced externality of existing technologies which wind can help to avoid); and security of supply.

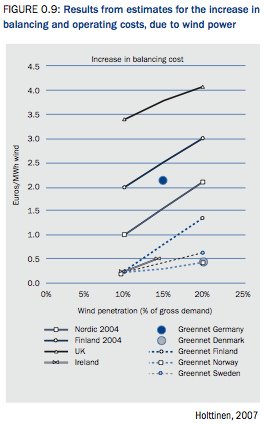

Intermittency and balancing costs

A traditional argument against wind is that its availability is variable and cannot reliably fulfill demand. Readers may be surprised to find this aspect listed here as an externality – but that’s what it is. In a market, you are not obliged to sell; the fact that the electricity grid requires demand to be provided at all times is a separate service, which is not the same thing as supplying electricity – it is, instead, continuity of supply. But while wind is criticized for its intermittency, I never hear coal or nuclear criticized because the reserve requirements of the system need to be at least as big as the largest plant around, in case that plant (which is inevitably a multi-gigawatt coal or nuclear plant) curtails production. The market for MWh and the market for “spare MWh on short notice” are quite different, and the Germans actually treat them separately:

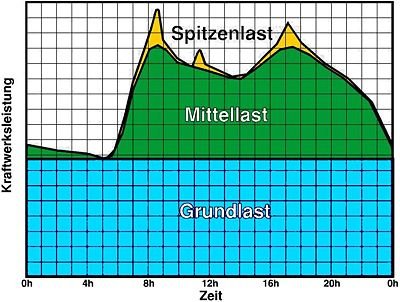

The Germans distinguish between permanent base load (i.e., the minimum consumption of any time which effectively requires permanent generation, “Grundlast” {in the graph above}, semi-base load {or the predictable portion of the daily demand curve, “Mittellast” in the graph above}, and peak/unpredictable demand (i.e. the short term variations of supply availability and demand – “Spitzenlast” {in the graph above}). Wind is now predictable with increasing accuracy with a few hours advance, and can, for the most part, be part of semi-base load. That is, low winds can be treated just like a traditional plant being shut down for maintenance: reduced availability of a given production facility, for which standard energy-planning strategies apply.

For contrasting views on this topic, you can read these two articles: Wind is reliable and Critique of wind integration into the grid on Claverton. The reality here is that the service “reliability of supply” is well-understood, and the technical requirements (having stand-by capacity for the potentially required volumes) are well-known. There is plenty of experience on how to provide the resource (“spinning reserves”, i.e. gas-fired plants available to be fired up; interruptible supply contracts with some industrial users who accept to be switched off at short notice). Experience and the relevant regulations have made it possible to put a price on that service.

In the case of wind, the cost of this service (which a wind producer pays to the grid operator) is estimated at 2-4 EUR/MWh, which is 5% or less of the cost of wind (essentially, amortized initial investment cost). And, given that the relevant regulations exist, this externality can be easily internalized – either added to the cost of producing windpower or deducted from the price that wind generators can get for selling their “naked” MWh.

Carbon emissions

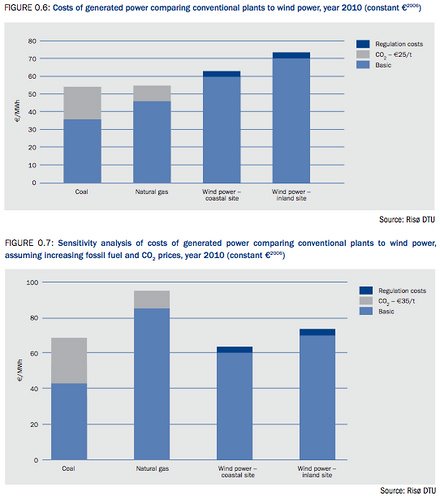

The second externality to mention is carbon emissions. In that case, it is not an externality caused by wind generation; it is an externality which is created by existing power generators, which is not properly accounted for yet today, but which wind generation avoids. In other words, there is a benefit for society to replace fossil fuel-burning generation by wind, but it is not ‘priced in’ yet (or, in other words, the indirect cost of coal-burning is paid by, for instance, the inhabitants of low-lying islands rather than by the consumers of that electricity).

Attempts to price carbon emissions are moving forward via the European ETS (emissions trading system) and the expected “cap-and-trade” mechanism in the USA. These require carbon-dioxide-spewing generators to pay for that privilege, which will be added to their cost of generating electricity (but not to that of wind, as it emits no carbon dioxide in the process).

The grey area in the bars above is the added cost of producing electricity from coal or gas for two different prices of carbon (note that the bottom graph also changes the cost of fuel, which increases the other component of cost for coal and gas). It has a significant impact on the net cost of production for these sources and on the respective cost-advantages of competing technologies. Note that the graph above includes the grid-related costs for wind, as discussed above, in dark blue.

It is legitimate to include the cost of carbon, as it is to include the cost of stand-by capacity, in the calculation of the cost of electricity. If we consider the power grid as a fully integrated system, then there is very little reason to include some externalities and not others – other, that is, than force of habit and lobbying by the incumbents who designed the rules around their existing generation mix.

Security of supply

A power plant is an investment that can last 25 to 50 years (or even more, as in the case of dams). Once built, it will create patterns of behavior that will similarly last for a very long time. A gas-fired plant will require supply of gas for 25 years or more (and the corresponding infrastructure, attached services, employees … and lobbyists). Given worries about resource depletion (usually downplayed) and about the unreliability of some suppliers (hysterically exaggerated, for example, by the “New Cold War” hype about Putin’s Russia), it is not unreasonable to suggest that security of supply has a cost.

This may be reflected in long term supply arrangements with firm commitments by gas-producing countries to deliver agreed volumes of gas over many years. However, given all the Russia-angst we hear in Europe, this does not seem to be enough (even though most supplies from Russia are under long term contracts). Wind, which requires no fuel, and thus no imports, neatly avoids that problem, but how can that be valued in economic terms? That question has no satisfactory reply today, but it is clear that the value is more than nil.

Another aspect of this is that “security of supply” is usually understood to mean “at reasonable prices.” Fuel-fired power plants will need to buy gas or coal in 10, 15, or 20 years’ time, and it is impossible today to hedge the corresponding price risk. Given prevalent pricing mechanisms, individual plants may not care so much (they will pass on fuel price increases to consumers), but consumers may not be so happy with the result. Again here, wind, with its fixed price over many years, provides a very valuable alternative: a guarantee that its costs will not increase over time. Markets should theoretically be able to value this, but ‘futures’ markets are not very liquid for durations beyond 5 years, and thus, in practice, they don’t do it. This is where governments can step in, to provide a value today to the long term option embedded in wind (i.e., a “call” at a low price). This is what feed-in tariffs do, fundamentally, by setting a fixed price for wind production which is high enough for producers to be happy with their investment today, but low enough to provide a hedge against cost increases elsewhere in the system. Indeed, last year, when oil and gas prices were very high, feed-in tariffs in several countries ended up being below the prevailing wholesale price: the subsidy proved its purpose.

Note that the regulatory framework will decide who gets access to that value: if wind is sold at a fixed price, it is the buyer of that power that will benefit from the then-cheap supply (and that may be a private buyer under a PPA, or the grid operator. Depending on regulatory mechanics, that benefit may be kept by that entity or have to be reflected in retail tariffs for end consumers). If wind producers get support in the form of tax credits or “green certificates”, it is wind producers that will capture the windfall of higher power prices. So the question is not just how to make that value appear, but also how to share it. Both are political questions to which there are no obvious answers, currently.

So wind power has value as a low-emissions, home-grown, fixed-cost supplier. It also tends to create significant numbers of largely non-offshoreable jobs, which may be an argument in today’s context. It also has, in a market-pricing mechanism, the effect of lowering prices for consumers, thanks to its zero-marginal cost. Its drawbacks, mainly intermittency, can be priced and taken into account by the system. (Birds/bat are not a serious issue, despite the hype; aesthetics are a very subjective issue which can usually be sidestepped by avoiding certain locations – the US is big enough, and Europe has the North Sea.)

Altogether, wind seems to be an excellent deal for consumers – and an obvious pain for competing sources of power, except maybe those specializing in on-demand capacity. In other words – sticking with mostly coal or nuclear is a political choice, not an economic one.

Source / European Tribune

Note that Jerome simply assumes that less fossil fuel would be burned as more wind is added to the grid. There are, however, no data supporting that assumption.

It appears that wind’s high variability requires the rest of the grid to respond in a way that does not save fuel.

One of the arguments I’ve seen most about current wind generation technology — and one in which I have a great deal of interest — is the potential ill effects on migrating birds, butterflies, or even birds going about their daily business.

There ought to be some way to shield rotating turbines from unwary creatures — of course, I think the same thing everytime I read about an airplane getting in trbole because a bird has been sucked into the turbine; can’t they cover them somehow with screens?? Until this issue is squarely addessed, wind technology will not command the full support of environmentalists as a group.

trouble — not “trbole” lol

Although this article explains the concept of “intermittancy,” it does not actually answer the question about its effect on supply to the grid. An American Electric Power speaker at a seminar last fall stated that electric utilities could not support more than 12% to 15% of their capacity in wind or solar resources because of the inconsistency of production, which is dependent on wind speed or hours of sunlight, as well as energy “density” in general. While those large “gigawatt” coal plants are rarely taken down on an unscheduled basis, the authors make the comparison of coal to wind without addressing the general non-reliability of wind generation.

Variability may pose a challenge initially, but could diminish as the number and locations of windfarms increase across suitable grids. A least a part of the answer, my friends, IS blowing in the wind.

The author only parenthetically glances at one of the central problems with this form of renewable energy, and that is the environmental and “green” costs of getting the electricity from source to market.

Using a large-scale industrial model for wind power production means the construction of hundreds of miles of high-voltage power lines, and in the USA (Europe increasingly buries these lines underground) that means huge lattice towers and so-called “monopoles” marching through whatever vestiges of rural landscape remain. Not very green at all, and the jury is still out on the health effects of living and working near the electromagnetic fields of such lines.

Just like there’s no “clean coal” as long as mountaintop removal coal mining provides the source material for coal-fired plants, I’d argue there’s no “clean wind energy” as long as it demands the construction of intrusive, landscape-destroying distribution systems.

Intelligent renewable energy sources will be local and decentralized. The money to be made, and the new economy to be created, will be in manufacturing the local and even household-level technology to produce that energy and distribute it locally in an environmentally responsible way.

All else is “greenwashing.”

See http://www.clearviewalliance.org for info about a group in Kimble County, TX currently mobilizing to head off construction of power lines through their scenic neighborhood.